Statistical Facts of Artificial Stock Market

The price emerged by the agent’s interactions is calculated by the excess demand in

each round, i.e.:

⎟

⎠

⎞ ⎜

⎝

⎛ ∆ = + − = ∑

N

i

i

t p p t p t x

1 ( ) ( 1) ( ) λ …(5)

where λ is the market depth or liquidity, the excess demand needed to move the price

by one unit. The market depth measures the sensitivity of price to fluctuations in excess

demand (Cont & Bouchaud, 2000).

As a summary of the model overview, we can see table 1 showing the value of

variables used in simulations.

Table 1

Initial Simulation Configuration

Parameters Value

Number of iteration 10,000

Number of agent (investor) 200

Formation fundamentalist-chartist-noisy 42-109-49

Chartist (h=30) – (h=60) – (h=100) 46-33-30

Stock owned by each agent 10

Money owned by each agent IDR 20,000

Market Depth (1/ λ ) 10

Basic price each stock IDR 5,000

- Simulation Results

We do several simulations in our artificial stock market in order to have some

understanding points of what we discover in previous work on statistical properties of

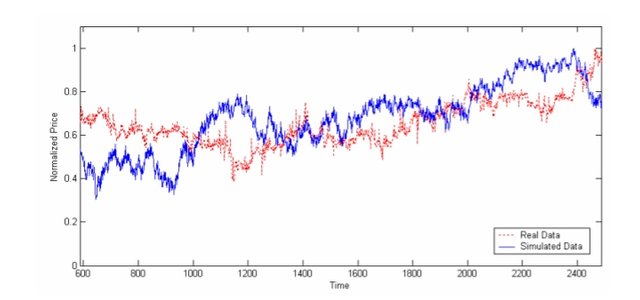

Figure 1

The simulation result compared to the real normalized hourly price data of a dominant indivi