What is LendingClub all about? A little explanation of P2P lending

What is LendingClub?

If you haven’t lived under a rock for the past few years you should sort of know what peer-2-peer lending is about and in particular you have probably heard of LendingClub, the leading platform that provides P2P lending.

LendingClub runs a platform that markets unsecured loans to borrowers. It sells the loans of those who have been approved to a variety of investors. As a classic example of the emerging sharing economy, the platform connects thousands of individual and business borrowers with regular people willing to fund their loans. In doing so, it eliminates the need for borrowers to approach traditional banks and credit unions (whose lending standards may be much more stringent than LendingClub’s) to obtain financing.

Ok, but how does it work? (Business model)

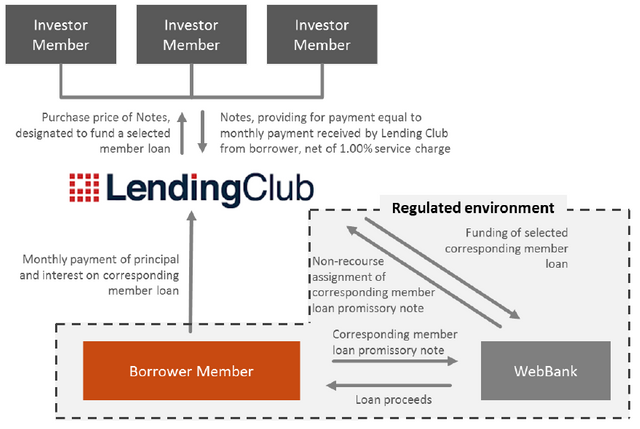

At first sight, it’s a one-to-many relationship between the borrower and investors. A $1000 loan of a borrower will be made up of a multitude of $25 denominated Notes (and integral multiples of $25) funded by investors.

These loans range from $1,000 to $35,000 in size and have terms of 36 or 60 months. Borrower interest rates range from about 6.75% to about 30%, depending on credit score, credit history, and past borrowing record with LendingClub.

LendingClub doesn’t tie its rates to an index such as Libor, but it advises that rates may rise or fall depending on “market conditions”, in other words, prevailing interest rates. LendingClub also uses its lenders’ funds to make unsecured business loans with terms of 12, 24, 36, 48, or 60 months and principals of $15,000 to $100,000.

But how does it really work? (Loan platform)

Based on an interview in 2013, the former CEO, Renaud Laplanche (who resigned on May 9, 2016), claims that LendingClub “[does] the matchmaking and perform important risk management functions. [The company] underwrite, price and service the loans on behalf of investors.”

But by looking a little deeper into it we realize that it is not exactly as he explains: according to the IPO filing, LendingClub has $4.59 billion worth of loans on its books (as of Dec 2015). The actual loan origination is done by WebBank, a Utah-chartered financial institution that sells the loans to LendingClub. So there's nothing peer-to-peer about it.

The company is an intermediary between a bank and institutional investors, a structure that moves the lending business out of a regulated environment into an unregulated one.

WebBank, established in 1997, has indeed all the same lending capabilities as LendingClub does, but its regulators would never allow it to take on the $4.59 billion in assets it has helped generate for LendingClub (the current millions in delinquent loans amount alone would be enough to eat through its capital). LendingClub can do so because it is not a regulated bank. Rather, it relies on regulated banks "to originate all loans and to comply with various federal, state and other laws," according to the IPO filing.

See, LendingClub doesn’t have (and doesn’t want) a banking license, so it relies on Webbank to originate loans. Turning to a third-party to create the loans lets them avoid regulatory costs, and being viewed as a technology company rather than financial firm improves their image with investors.

It takes about 48 hours for the platform to match a loan to investors / lenders that eventually end up funding the borrower. At that point, the platform can buy the loan note from WebBank and the funding is “transferred” to the lenders. Essentially, the regulatory license and the capital of the FDIC insured industrial bank is used for 48 hours and then this capital is replenished.

While Webbank remains relatively small for a bank, it is very profitable because it dominates the rapidly growing P2P lending (ROE is 5 times the current US bank average): WebBank collects interest on the money for that window of 48 hours and earns a fee from LendingClub.

There are a lot of ways in which LendingClub is not a bank, but the big one is that basically almost all of its liabilities are "notes and certificates," that is, just unsecured structured notes tied directly to specific underlying loans. Banks, on the other hand, are funded mostly by deposits and repo and other short-term senior borrowing. So:

- LendingClub's assets and liabilities are perfectly matched in duration (think: Asset-Liability Management completely automated): those notes and certificates mature when the corresponding loans mature. A bank, on the other hand, is in the business of borrowing short to lend long.

- LendingClub's assets and liabilities are perfectly matched in loss bearing: Every dollar that a borrower doesn't pay back to LendingClub is a dollar that LendingClub doesn't pay back to note holders. The note holders know going in that they bear the entire risk of loss on the underlying loans. A bank depositor expects to get her money back even if the bank makes some bad mortgage loans.

So what does this mean?

Well, this basically takes all of the risk out of LendingClub's balance sheet. Yes, its business has risks: It can make dumb investments or competitors can steal all its customers, etc.; and its debt (those notes and certificates) is risky, in that the borrowers might not pay it back. But all of the things that make banks scary don't apply. A run on LendingClub is not possible: nobody can pull their money out of notes or certificates. And if a lot of loans go bad, that will hurt the investors in those notes, but LendingClub as an entity won't be insolvent or even have any losses at all.

In any useful sense, LendingClub is a 100 percent equity-funded bank: every dollar that it lends comes from long-term, loss-bearing investors.

Dear User known as @jurisnaturalist

Steemit has a BOT problem! Your Vote Counts... Maybe

https://steemit.com/steemit/@weenis/bots-steemit-s-first-community-based-decision-on-bots-your-vote-counts-to-be-or-not-to-be-details-inside

Dear User known as @jurisnaturalist

Steemit has a BOT problem! Your Vote Counts... Maybe

https://steemit.com/steemit/@weenis/bots-steemit-s-first-community-based-decision-on-bots-your-vote-counts-to-be-or-not-to-be-details-inside

Hi. By providing a line of credit based on factors such as income, employment history, and banking history, Snapfinance opens the door to those who would otherwise have difficulty making necessary purchases. In addition, they have a large selection of partner stores, where every customer can find all the goods he needs. Using their services is very simple, and if difficulties arise at any stage, then snapfinance customer service is always there and will provide the necessary assistance to everyone.