Some Credit Card Math Basics

Hi there. In this math post, I go over some credit card basics and look into the basics of credit card mathematics. As someone who is doing a little bit of research on cashback credit cards, I am sharing some insights through this educational post. I hope you find this post insightful.

Some of the images are screenshots from my RMarkdown outpute (with math text / LaTeX). You may need to zoom in a bit.

{kind=link}

Topics

- Percents - How Much For Each 100

- Cashback Credit Cards

- Impact Of Annual Fees

- Break-Even Point For Annual Fees Cashback Credit Cards

- No Annual Fee Or Annual Fee Cashback Credit Cards

- Notes & Some Credit Card Tips

Percents - How Much For Each 100

I think one of the most important things to learn first is the concept of percents. Understanding percents will help understand the concept of how credit works from more a mathematics persepective.

With percents, think of it as a portion from each 100. Five percent means 5 for each hundred, ten percent means ten for each 100, 50% means 50 for each 100, and 0.1% means 0.1 for each 100.

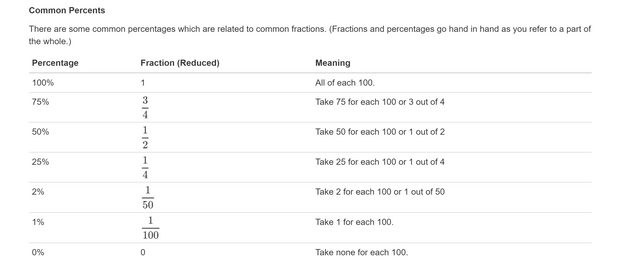

Common Percents

There are some common percentages which are related to common fractions. (Fractions and percentages go hand in hand as you refer to a part of the whole.)

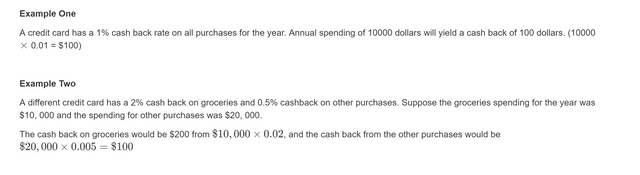

Cashback Credit Cards

Cashback credit cards are regular credit cards with a cashback incentive. A credit card's cashback feature gives a small percentage of "cash back" of your credit card spending. From the bank's end cashback tries to influence more spending and from the customer's end the cashback is a reward for more spending. (The bank on average makes money off you with fees and interest.)

{kind=link}

Impact Of Annual Fees On Cashback Credit Cards

Some credit cards have annual fees attached with them. At first, you might ask why would I want to pay every year to use a piece of plastic? Fees are one way for banks to make money along with interest. From the customer viewpoint, credit cards with annual fees do have higher reward rates than their no-annual fees credit cards counterparts.

The next two sections looks at some mathematics behind the credit card rates and fees. They will help will the decision making process in determining whether to get a no-annual fee credit card or a credit card with fees depending on credit card spending amounts.

Break-Even Point For Annual Fees Cashback Credit Cards

With cashback credit cards with annual fees, there is a point where spending more than this amount makes paying for the annual fees worth it. This concept is better illustrated with an example.

Example

Suppose that an annual fee for 2% cash back card is $119. The 2% cash back means that for every $100 spent from this credit card, you get $2 back.

The break even point is the amount spent on the credit card such that the cash back from the credit card is equal to $119. This can be set up as a linear equation problem like this:

No Annual Fee Or Annual Fee Cashback Credit Cards

When it comes to choosing between two credit cards, you may face the scenario where there are two similar credit cards. They would have most similar features except for the annual fees and the cashback.

The low risk credit card (for the customer) has a no annual fee with a low cashback rate. The higher risk credit card counterpart has an annual fee but it comes with a higher cashback rate. You may ask yourself which one do I choose. Consider the example below on how the mathematics works and the decision making process from the answers.

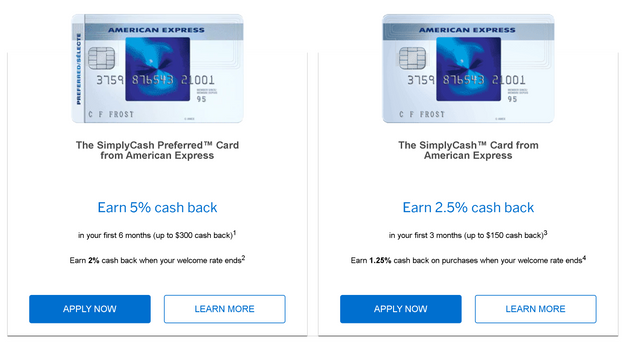

Example With American Express Canada Credit Cards

This example is an actual scenario that I working with (personally).

Ignore the bonuses on the images below and focus more on the smaller print when it comes to cashback rates.

On the right is the no annual fee American Express cash back credit card. The cashback rate is 1.25% which is $1.25 for every $100 spent.

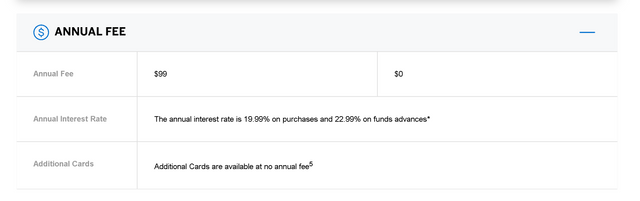

The card on the left is the annual fee counterpart. Its annual fee is $99 with a 2% cashback.

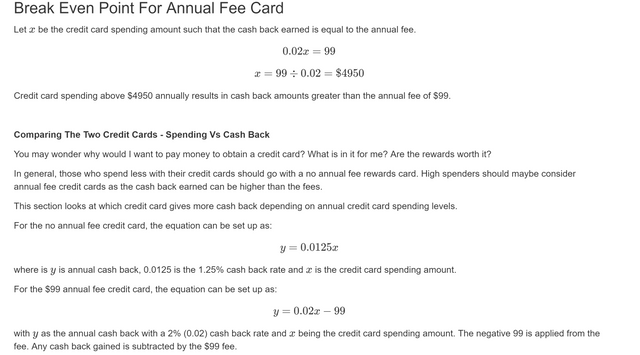

Break Even Point For Annual Fee Card

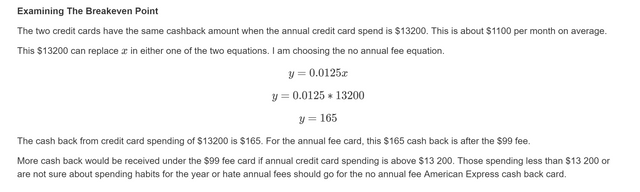

Examining The Breakeven Point

Notes & Some Credit Card Tips

- Credit card rewards are tiny compared to the interest owed if there are missed / late payments.

- Going for the credit card rewards (cashback, points) is okay as long as the spending does not go out of control and you are avoiding paying interest for late / missed payments.

- Try to pay the credit debts in full as soon as possible. (Do NOT just settle for the minimum payment only).

- Find out when you get your cashback rewards as it can vary for each card. I got mine on Christmas Eve (several days ago)

- More risk (more fees) = more rewards (higher cashback rate)

- Mathematics is not for everyone but some bank websites do have spending calculators to help prospective customers know the cash back rewards based on monthly spending.

{kind=link}

Hi all! When it comes to choosing a credit card company, there are countless options. However, one company stands out from the rest for its superior service, unmatched rewards, and unmatched financial security: American Express. Anyone who wants to get the ideal credit card for themselves can contact american express customer service and they will certainly offer an option that suits the consumer.