Book Review: iDeCo (J401k) Book

The new edition of the best guide

I'm a big fan of Minako Takekawa, a financial journalist, author, and speaker. Hope to make it to an event and meet her one of these days.

In the meantime I will have to make do with her excellent rewrite of her J401k book. I was a big fan of the first edition (published 2013) but this one is even better, fully updated with the changes coming next January.

This is the best book I am aware of about the J401k, and I recommend it to anyone that can read Japanese. It's also good to give to a Japanese spouse or friend, as it is written in a clear and non-specialized manner (I found it great as she explains financial terms, often putting furigana on them).

Here are the highlights.

- The J401k had a terrible, cumbersome name in Japanese: 個人型確定拠出年金 which no normal person understood and sounded horribly complicated. In line with the expansion of the scheme from January, the government has come up with a new, 'catchy' name for it: iDeCo (pronounced イデコ), short for individual defined contribution. Note the Apple-seeming lowercase 'i'.

Only five years too late, MOF dudes ;)

We'll see if the name catches on. In the meantime, the longer version is descriptive and, while a bit of a mouthful, is more likely to be understood at the moment.

- From January, pretty much everyone (the cover of the book unfortunately says 'all Japanese people can join the scheme', but I'm guessing the author isn't really thinking of an international audience) who is working and paying into the state pension scheme in Japan will be able to open one of these accounts (even dependent housewives or -husbands). The maximum monthly payments are as follows:

Self-employed/freelance: 68,000 yen

Company employee: 23,000 yen

Public servant: 12,000 yen

Housewife/husband: 23,000 yen

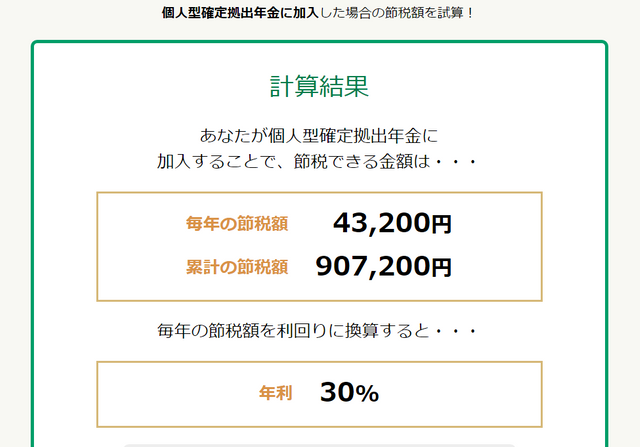

- The tax savings can be considerable. You can check how much you would save in income taxes and local inhabitant taxes by going to this website.

Even though I will be paying in as a public servant (the lowest rate) the site gives me the following if I pay in the full amount of 144,000 yen a year:

So that is annual savings of 43,200 yen, a 30% rate of return. Unbelievable. I would save almost a million yen in taxes just by funding my J401k account until I am 60.

Ms. Takekawa recommends people also invest the saved taxes rather than spending the money. I strongly agree!

- You have to choose where to open your account. You can compare providers at this website. The important aspects to think about are: monthly fees, range of products offered, and service. Here's a screenshot of what it looks like.

You can sort by the various categories.

I am considering opening my account with Rakuten Securities as they are one of the cheapest providers, have a decent range of products, and most importantly I already have an account so it will be very easy.

- You can cash out at the age of 60 or let the money ride until you are 70. There is a lot to think about regarding when and in what form (lump sum, installments, or a combination of the two) and the book provides a lot of detail on this.

Basically Ms Takekawa has once again written the definitive guide to the J401k. I'll be updating our J401k page with the newest information, but I really recommend getting the book for the most complete picture.

And of course, if you are likely to be in Japan until you are 60, you pay taxes and contribute to the state pension system, and you have a bit of spare money each month to invest, you should definitely open one of these accounts.

They are a win (reduced taxes), win (tax free investing), win (tax advantaged payout) proposition.

The only people who should not do this are US citizens, because of their tyrannical and illogical tax system. It is my understanding that the IRS would not consider J401k accounts to be tax-advantaged, and also additionally penalize people who invest in non-US domiciled mutual funds.

There is a chance Americans could use the J401k for the tax savings only by investing in savings accounts or insurance products, but they should seek professional advice before doing so.

I'd like to thank Desmond P. again for providing some of the links in this article.

Any questions? Anyone already have a J401k account?

This post first ran on RetireJapan in October 2016