The Coming Flood (Six Reasons the Global Economy is Doomed)

(I know, that’s a tsunami. But you get it.)

We’re all on borrowed time people. Literally.

Over the past few months, it’s becoming increasingly clearer to me that, economically, we’re headed on a downward spiral the likes of which we have never seen. I don’t mean to come across as a catastrophist, (improvised word) but every second we’re not in a recession is starting to feel like ever thinning ice for the global economy. This collapse however, is not going to spell Armageddon for everyone. In fact, a very alert, very lucky, very exclusive, select few who notice these signs early enough and are adequately prepared stand to be enriched greatly when the economy breaks down, and future coming pieces, I’ll explain why.

Now, for those new to my work, this isn’t my typical format. I generally keep conversations on the abstract, archetypal domain, usually with regards to religion, anthropology, psychology, and spirituality, with a little personal experience thrown in there for fun. However, I find that this particular topic dovetails nicely with the Flood theme that runs through the next Biblical story I plan to cover, Noah’s Ark. So, it’s time to bring these stories down to earth with an analysis on why the global economy is all but scheduled for a disaster.

Factor One: We’re overdue for this.

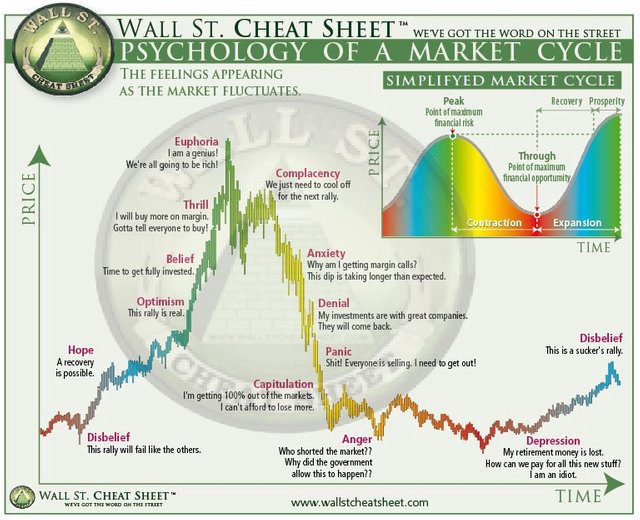

(Looks like we’re somewhere between complacency and anxiety)

Many of you with a bent for finance and economics have already seen this picture a thousand times. It depicts the pulsating nature of virtually every economic market in existence. What makes this chart so powerful is that it’s not a map of financial markets at all. It’s a map of human psychology. We all know the ebb and flow nature of life, the euphoric highs and the catastrophic lows. It’s just a fact of the human experience; if and when things get good, they don’t stay that way for long. As such, in finance, there is no such thing as continued or sustained growth. It’s built into the nature of any market to crash every now and again, because it’s the nature of the human mind to panic when things get too hot. This is doubly true when it comes to money.

Here are some numbers on this trend for reference.

We (the United States) are at a near fifty year low for unemployment rates (3.7 percent).

The economy has added 3.2 million new jobs, (though the job creation under the previous administration was a bit faster).

The stock market in recent years has been strong,and getting stronger. The Dow Jones set an all time closing high of 26,828.39 in October of this year, however just this last week it did slip a bit, which sparked some nervous pencil tapping among some analysts. That’s why I’ve concluded that we’re somewhere in the complacency to anxiety phase in our psychological economy.

Another thing to note about the stock market is that it has been massively inflated by corporate stock buybacks after congress passed legislation to relax the corporate tax rate, which will only cost the economy a paltry $2 trillion.

“According to data from Goldman Sachs, companies in the S&P 500 have authorized $205 billion in buyback programs thus far this year, which represents growth of 48%.”

Not bad, GOP!

I don’t want to go off on a tangent here, but slashing taxes for corporations is NEVER a good idea for stimulating the economy, creating jobs, or whatever other crackpot theories its proponents use to justify it. The function of a corporation is to generate profits for its shareholders. That’s it. It’s actually a legal requirement for them to do so, so, the moment corporations get their hands on a little extra cash, you’d better bet your sweet derriere they’re going to use that money to buy back their own stock, and inflate prices. Why on earth would they do anything else?

It seriously grinds my gears that so many people were utterly duped into believing that the corporations were going to just use that extra money to dole out financial hand-me-downs’ and create more jobs. That’s not how wealthy people think. And furthermore, this exact pattern has literally happened a little over a decade ago.

I could go on about this, but I’m becoming rather ornery, and I’ve come down with a harsh cold. So, for now, let’s put a pin in it.

The point is, we’ve been riding the Obama Train of Accelerated Economic growth for far too long now, and we need a market correction.

(Choo, Choo…)

Factor Two: Liquidity!

(The drip is starting to slow.)

We need more money, not assets! Our assets to liabilities ratio is looking horrendous, to say the least. The national deficit has found an all time high at 21 trillion, and our liberal (ironic word, considering this ploy came from the political “conservatives”) deficit spending is only worsening the balance sheets. We simply don’t have enough liquid cash on hand to cover our assets, (wink) and dropping trillions down the drain on a whim is about the worst thing we could’ve done in response to that.

If every single lender we rely on decided to call in the loans we’re accruing, we’re going to have to default, and our country will go bankrupt. Furthermore I see zero political effort to mitigate this trend. Instead, in recent years, the problem has only worsened.

But that’s all well and good thanks to factor three.

Factor Three: We cannot (and don’t even plan to) pay off our massive debts.

(When the creditors come knocking, we will have already skipped town. Knock.)

The economy is massively over-levered in just about every way you can imagine. Student loan debt is at an all time high, so young, college-educated chaps and chappettes looking to to establish their lives are saddled with near-unbearable amounts of debt right out of the gate. This makes it incredibly hard say, to go out and buy a home for your budding family, unless of course, you could borrow the money from someone...

Oh, and while we’re on that topic, real estate prices are over inflated, a consequence of the slashed tax rate, and they’re also mired in debt. If you thought banks and institutions were just done with their predatory lending tactics that crashed the last economy, think again. They’re just doing it through shell companies now.

The stock market is also essentially built on debt, due to our penchant for leveraged trading, which is, in layman’s terms, borrowing money that you do not have to go off and invest, which is a brilliant way to get fabulously rich overnight (or lose your shirt today). By the way, banks do this all the time, in case you thought your money was safe with them. Hah.

Credit card debt is at record numbers too. A quick Google search reveals the average American has about $6,375 in credit card debt, contributing to the astronomical $1 trillion we as a nation owe to creditors. But then again, as a newly-fledged salary slave with ludicrous student loan and homeowner’s debt, how else are you going to pay for the luxury goods that help you feel like a success? Now, I’m not knocking the people living this lifestyle, just pointing out that our current economic system is set so that the average American lives a life of modern indentured servitude, working to pay off the debts their government has accrued, which, as it turns out, still won’t get paid off. Yuck.

Trust me, there’s more.

Factor Four: The Fed has basically planned this.

(The Federal Reserve. Where dreams happen.)

Remember how I mentioned that the economy, powered by the human mind, travels in cycles? Well, much of that fluctuating movement has been manufactured, or forced upon us by the Federal Reserve. Since we went off the gold standard, money printing no longer has a cap, and our good buddies over at the Federal Reserve are definitely enjoying their unlimited printing power. Unfortunately for you, that means your dollar is losing value at a rate of 3 percent each year, and your dollar last year will only net you 97 cents today, with no clear path to improvement.

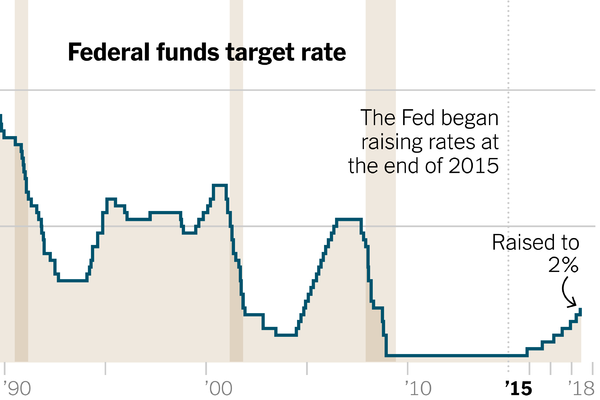

They’re also very sneaky with their rates.

Now, every time the Fed tickles interest rates, the economy wobbles, sometimes for the better, but more often not. As you can see, around ’08, the Fed slammed interest rates down to near zero to encourage borrowers and stabilize businesses. The Fed had to do this because, after the housing bubble, the economy was spiraling out of control. In a curative effort, the Fed dropped their rates so that borrowers could get back on their feet again. But don’t paint the Fed as the heroes of this story just yet. Notice how, prior to the housing bubble, the Fed had been hiking up interest rates in tandem with the growth of the irrationally inflated economy, peaking in ‘08. EVERY single time the Fed hikes interest rates, the economy recedes, and then they have to mop it up by lowering rates again to re-stabilize it. So, in effect, they’re just “solving” the problem they’re creating (sort of).

Also, note the current trend of federal interest rates, no bueno.

Factor Five: We’re hyperlinked to sht.*

“We live in a global economy” is a nice way of putting it. What that means is there are no longer any isolated economic systems. Each contributor is unsettlingly reliant on the health and prosperity of every other contributor, so, if too many pieces tumble, the entire system collapses. It works like this. The entire world financial system is like a living body, with the United States (for some reason) at the center, it’s beating heart. If too many peripheral systems crumble, it has a chain effect which will inevitably reach the core. Once the heart fails, the entire system goes under, even the brain (Europe) can’t function on its own.

Now what caught my attention (and virtually no one else’s) is that smaller economies are starting to fade, or just completely disintegrate.

Masood Ahmed, former top official at the International Monetary Fund, and current president of the Washington D.C. think tank for global development had this to say.

“…consider that of the 59 countries the IMF classifies as “low-income developing countries,” 24 are now either in a debt crisis or at high risk of tipping into one. “That’s 40 percent of poor countries,” says Ahmed, “and it’s nearly double the number five years ago.”

The Republic of Congo and Mozambique are both in a bit of a pinch, each defaulting on their loans, a process that could take decades to recover from. The Venezuelan economy has shrunk by half, with interest rates jacking prices up (I kid you not) one million two hundred ninety nine, seven hundred percent. Not a made up number folks, they’re getting crushed out there. By the way, 5 million Venezuelans are projected to pack their bags and depart from their homeland in 2019 alone. Say goodbye to the workforce.

(Venezuelan Exodus, and you thought your life was stressful.)

Now, as of yet, we haven’t felt the sting of these economic collapses because of an unbelievably thick buffer of wealth and privilege, but trust me, the storm is headed our way.

Finally…

Factor Six: The dollar will die.

(And you can help it!)

What happens when you take an over-inflated, over-levered economy based on a fiat currency with zero resources backing it, cheated and disgruntled citizens, and a nasty jump in interest rates? Nothing terrible, unless you were to link it to a crumbling global economy with debt crises proliferating left and right. That would be trouble.

Leaving the gold standard wasn’t just a moderately bad idea. It was the mother load of all ill-conceived, horrendously executed plots. The whole point of a dollar was that it was a promissory note, an IOU. U.S. dollars were the receipt you got when you made a corresponding bank deposit in gold. During the Golden Days (pun intended) you could literally take your dollar bills to the bank, and receive their weight in gold. That afforded the economy some authenticity, since the banks couldn’t just spend or loan out cash willy-nilly without having an equivalent store in something tangible.

Now, without a corresponding commodity backing it, the dollar has become an IOU with no worth(I Owe You Nothing…). If the economy collapses, oh well, tough luck for our lenders, and our citizens for that matter. We’ve got nothing to show for it. And, since there’s no cap on the money we can now pull out of thin air,we can just puff and puff and puff this thing until it pops.

The only think keeping the dollar afloat is the vast integrated network of banks and institutions that transact in it. However, once a critical mass of Americans realize their bank notes are a unit of the massive debt their banks have incurred, and that they’re the ones footing the bill, the U.S. dollar is a goner. Luckily enough, there’s a new disruptive asset class countless central banks and institutions are building an infrastructure around, so when the dollar bubble pops, there’s a space for all the frozen, debt-based, illiquid capital to flow into.

To put this in perspective, most Americans, if not most people, are financially screwed. With all manner of debt reaching for the roof, no plan to pay it, peripheral economies shattering, and a whole host of other contributors, in the next 3–5 years, we’re going to see a global financial meltdown to end all meltdowns. Honestly, many of us won’t make it.

The rich however, as always, will be just fine. As I’ve said, they’re quietly but steadily gathering resources and building an infrastructure around the next economic hotcake to hit the mainstream. They’re building an Ark. And you should too. Disregard all the tough talk you’ll hear about the dollar doing just fine, and the stock market booming, and pay attention to the signs. Pay attention to the big money, the Central Banks, billionaire corporations, and powerful financial institutions. What are they all raving about? What assets are they accumulating and prepping for? They’ve got their eyes open, they’re all well aware of the direction the global markets are heading, and, just like the short sellers in ’08, they stand to profit, not lose from the impending disaster.

If you want to be wealthy, play the wealthy man’s game.

Look out ahead 3–5 years from now, and behind you into the foreseeable past. No one in the mainstream is really paying attention to these things right now, so you’re ahead of the curve.

(Oops)

Most people, if they even invest, buy the present and sell the future. But you can be different. If you’ve got you’re eyes open today, you’re unbelievably fortunate, because you can make the proper arrangements, and ride the next big economic wave, wherever it goes.

Ignore the general public, and emulate the financial elite. That’s how you’ll survive, and even thrive, in the coming flood.

(That’s a Badass BeefCake Boat Builder right there.)

See you on the other side!

Omg why did I have to start reading it! I love it but I just noticed how long is your post :) Gonna have to finish later on. Just before bedtime.

Great piece of work @unchartedself

Yours

Piotr

And done. Read it all. I had to stop few times because I started feeling down and depressed.

Great piece of work @unchartedself

Yours

Piotr

Thanks! You're awesome for following up like this on everyone's work, keep it up!

Also, since you're into crypto, no need to be depressed, you're an early adopter in what will be the financial asset of the future!

Ciao!

Again, big thx for being so responsive @unchartedself

Also please allow me to invite you to visit my latest post (my last one in 2018). Together with few friends we decided to organize small charity event "Santa Venezuela" and hopefully we can count on your help. There are many ways of helping our venture :)

Have a great Xmas :)

Piotr

Dear @unchartedself

I just decided to visit your profile and check out your latest content only to notice that you didn't blog in quite a while already.

Hope you didn't give up completely on Steemit?

Cheers, Piotr

Dear @unchartedself

I just visited your account to see if you posted anything new lately and I see that you're taking a break?

Hope you're not done with Steemit and you will be back with some interesting publications soon :)

Yours

Piotr

Congratulations @unchartedself! You received a personal award!

You can view your badges on your Steem Board and compare to others on the Steem Ranking

Vote for @Steemitboard as a witness to get one more award and increased upvotes!