Why A Dollar Collapse Is Inevitable

Content adapted from this Zerohedge.com article : Source

The 1930s and 1970s were tough for the US Dollar. From this analysis, we are heading to a period where the drop in the dollar will be worse than either of those two periods.

Authored by Alasdair Macleod via GoldMoney.com,

"Naturally, the smooth termination of the gold-exchange standard, the restoration of the gold standard, and supplemental and interim measures that might be called for, in particular with a view to organizing international credit on this new basis, will have to be deliberately agreed upon between countries, in particular those on which there devolves special responsibility by virtue of their economic and financial capabilities."

General Charles de Gaulle, February 1965

We have been here before – twice.

The first time was in the late 1920s, which led to the dollar's devaluation in 1934. And the second was 1966-68, which led to the collapse of the Bretton Woods System.

Even though gold is now officially excluded from the monetary system, it does not save the dollar from a third collapse and will still be its yardstick.

This article explains why another collapse is due for the dollar. It describes the errors that led to the two previous episodes, and the lessons from them relevant to understanding the position today. And just because gold is no longer officially money, it will not stop the collapse of the dollar, measured in gold, again.

General de Gaulle made himself very unpopular with the international monetary establishment by holding the press conference from which the opening quote was taken. Yet, his prophecy, that the gold exchange standard of Bretton Woods would end in tears unless its shortcomings were addressed by a return to a gold standard, turned out to be correct shortly after. What the establishment did not like was the bald implication that it was wrong, and that the correct thing to do was to reinstate the gold standard. Plus ça change, as he might say if he was still with us.

Those of us who argue the case for a new gold standard, and not some sort of half-way house such as a gold exchange standard to address the obvious failings of the current monetary system, are in a similar position today. The first task is that which faced General de Gaulle and Jacques Rueff, his economic advisor, which is to explain the difference between the two.[i] It is now forty-seven years since all forms of monetary gold were banished by the monetary authorities, and today few people in finance understand its virtues.

Furthermore, in the main, historians educated as Keynesians and monetarists do not understand the economic history of money, let alone the difference between a gold standard and a gold-exchange standard. These similar sounding monetary systems must be defined and the differences between them noted, for anyone to have the slimmest chance of understanding this vital subject, and its relevance to the situation today.

Defining the role of gold

To modern financial commentators, there is little or no significant difference between a gold standard and a gold exchange standard. Keynes's famous quip, that the gold standard was a barbarous relic, was made in his Tract on Monetary Reform, published in 1923, before the gold exchange standard really got going, yet it is quoted as often as not indiscriminately in the context of the latter.

Yet, they are as different as chalk and cheese. The gold exchange standard evolved in the 1920s as America and Britain went to the aid of European countries, struggling in the wake of the Great War. It allowed the expansion of national currencies under the guise of them being as good as gold. It was not. In modern terms, it was as different as paper gold futures are to the possession of physical gold today.

A gold standard is commodity money, where gold is money, and monetary units are defined as a certain fixed fineness and weight of gold. The monetary authority is obliged by law to exchange without restriction gold against monetary units and vice-versa, and there are no restrictions on the ownership and movement of gold.

Under a gold exchange standard, the only holder of monetary gold is the issuer of the domestic monetary unit as a substitute for gold. The monetary authority undertakes to maintain the relationship between the substitute and gold at a fixed rate. Only money substitutes (bank notes and token coins – gold being the money) circulate in the domestic economy. The monetary authority exchanges all imports of monetary gold and foreign currency into money substitutes for domestic circulation at the fixed gold exchange rate. The monetary authority holds any foreign exchange which is also convertible into gold on a gold exchange standard at a fixed parity, and treats it to all extents and purposes as if it is gold.

The essential difference between a gold standard and a gold exchange standard is that with the latter, the monetary authority has added flexibility to expand the quantity of money substitutes in circulation without having to buy gold. A gold standard may start, for example, with 50% gold and 50% government bonds backing for money units, but all further issues of monetary units will require the monetary authority to purchase gold to fully cover them. This was the monetary regime in Britain and many other countries before the First World War. As stated above, gold exchange standards evolved after the First World War, in the early 1920s.[ii] It was the taking in of foreign currencies, also on gold exchange standards themselves, and booking them as if they were the equivalent of gold, that allowed central banks to expand the quantity of monetary units domestically. To understand how this operated in practice requires us to work through an example between two countries on gold exchange standards. We will take the entirely hypothetical example of two countries, America and Italy, both of which have monetary gold in their reserves and operate on a gold exchange standard.

America lends Italy dollars by crediting its central bank's account at the Fed with the dollars loaned. But while ownership has changed to Italy, dollars never leave America. And dollars, when drawn down by the Banca d'Italia are recycled into America's banking system.

The economic sacrifice to America of lending money to Italy is therefore zero. America has simply created a loan out of its own currency, and in the process increased the quantity of dollars in circulation. And because in practice Italy does not encash dollars for gold, America expects to preserve its gold reserves.

Meanwhile, The Banca d'Italia has expanded its balance sheet by the inclusion of America's dollar loan to it as a liability, and the dollars themselves as an asset regarded as the equivalent of gold. Because dollars are not permitted to circulate in Italy's domestic economy, they can be used by Banca d'Italia, either to settle other foreign obligations, or as a gold substitute to back the issue of further lira. Meanwhile, the Banca d'Italia's dollars are reinvested in US Treasuries, which give a yield. Banca d'Italia has little incentive to exchange its dollars for physical gold, because gold yields nothing and is costs to store.

If Banca d'Italia uses dollars to discharge a foreign obligation with another country, that third party will also end up investing the dollars gained in US Treasuries, assuming it also prefers yielding assets to physical gold. Alternatively, if the dollars are used by the Banca d'Italia to back an increase in the quantity of lira or to subscribe for government debt, the effect in the domestic Italian economy is an inflation of prices.

Therefore, the effect of a gold exchange standard is the opposite of a gold standard. A gold standard puts the requirements for the quantity of money in circulation entirely in the hands of the market, to which the central bank mechanically responds. A gold exchange standard allows a lending central bank to inflate its money supply through inward investment, and a borrowing central bank to inflate its money supply on the presumption the monetary substitutes borrowed to back it are monetary units of gold.

The gold exchange standard in the 1920s

After the First World War, both sterling and dollars were made available under the Dawes Plan of 1924, which provided non-domestic capital for Germany after her hyperinflation. France suffered a currency crisis in July 1926, which was successfully dealt with by the Poincaré government through raising taxes. The Bank of France was then enabled to borrow dollars and sterling and to issue francs and subscribe for government debt.

To summarise, these loans bolstered the balance sheets of the Reichsbank and the Bank of France, which invested the sterling and dollars borrowed in gilts and Treasuries respectively. If instead France and Germany had taken gold under the gold exchange provisions, they would have had an asset with no yield, though France did opt increasingly for some gold towards the end of the decade and beyond – by December 1932 she had accumulated 3,257 tonnes. So, by lending their monetary units, the creditor nations achieved finance for their own governments, as well as providing capital for foreign central banks. It was seen to be a win-win for all the central banks involved.

The accumulation of dollars in foreign hands from 1922 onwards accompanied and fuelled bank credit expansion in the US. This gave the roaring twenties an inflationary impetus, dramatically reflected in its stock market bubble. However, the increasing quantity of dollars in foreign ownership became an accident waiting to happen. There had been a mild thirteen-month recession from October 1926 to November 1927, after which the stock market boomed. The Fed was compelled to reverse earlier interest rate cuts and increased the discount rate from 3 ½% to 5% by July 1928.

French investors began to repatriate capital en masse, and the Bank of France's gold reserves rocketed from 711 tonnes in 1926 to 2,099 tonnes by 1930.[iii]The gold exchange standard had spectacularly failed, and redemption of dollars for gold, being deflationary, exacerbated the Wall Street Crash. It certainly rhymed with Robert Triffin's dilemma: the export of dollars into foreign ownership was monetary magic, until it reversed at the first sign of trouble.

The gold exchange standard of Bretton Woods

In 1944, the monetary panjandrums of the day, led by Harry Dexter-White for the US and Lord Keynes for the UK, designed the post-war gold exchange standard of Bretton Woods. No doubt, Dexter-White fully understood the advantage to the US of forcing all countries to accept dollars with a yield, or gold with none. When American payments abroad exceeded receipts, the difference was generally reflected in dollars issued to foreign central banks, kept on deposit in New York, or invested in US Treasuries.

Throughout the 'fifties, America recorded a surplus on goods and services, which declined as European manufacturing recovered. But other factors, such as investment abroad and the Korean war resulted in an overall balance of payments deficit totalling $21.41bn, the equivalent of 19,024 tonnes of gold at $35 per ounce. However, US gold reserves declined only 4,457 tonnes between 1950 and 1960, which tells us that the balance was indeed invested in US bank deposits and US Government notes and bonds.

The respective figures for the 1960s were total payment deficits of $32bn, the equivalent of 28,437 tonnes of gold, and an actual decline in gold reserves of 5,283 tonnes.

The accelerating increase of foreign ownership of dollars over these two decades meant the world, ex-America, was awash with dollars by the mid-1960s. By the end of that decade, America's gold reserves had declined from 20,279.3 tonnes in 1950, two-thirds of the world's monetary gold, to 10,538.7 tonnes, 29% of the world's monetary gold in 1970.

The effect was to remove trade settlement disciplines on net importing nations, and to cause inflation in net exporting nations, the opposite of the disciplines of a pre-WW1 gold standard on global trade. It was this effect that was central to the second Triffin dilemma, whereby dollars became wildly over-valued in gold terms through their excessive issuance.

In the mid-sixties, Washington became increasingly alarmed that foreigners weren't playing by the assumed rule that they should take dollars and not redeem them for gold. By then, France and Germany between them had increased their gold holdings from 487.1 tonnes in 1948 to 7,089 tonnes at the time of de Gaulle's press conference. General de Gaulle's press conference, from which this article's opening quote is taken, had touched some very raw nerves.

It was clear that the dollar, with the overhang of foreign ownership, had become horribly overvalued, and so should have been devalued, perhaps to over $50 or $60 per ounce, for a gold peg to stick. A devaluation of this magnitude might have been sufficient at that time to stem the outflow of gold.

Both Washington and American public opinion were set strongly against any devaluation. Instead, the London gold pool, designed to ensure the major central banks supported the Bretton Woods System, collapsed in 1968, when France withdrew from it. A dollar devaluation to $42.2222 shortly after was simply not enough, and in 1971 President Nixon suspended the Bretton Woods System, and the new regime of floating exchange rates that is still with us to this day began.

The situation today

Following the Nixon shock, official monetary policy towards gold was to ignore it, and to persuade other central banks and financial markets it was irrelevant to the modern monetary system. To this day, the Fed still books the gold note from the Treasury at $42.2222 per ounce, even though the price has risen to over $1300.

We can simplistically value the dollar in terms of gold, which is certainly a valid, perhaps the most valid approach. But to merely conclude that the dollar has collapsed since 1971, while true, side-steps an analysis that points to the risk that even today's value may still be too high. Furthermore, with the dollar acting as the world's reserve currency, all other fiat currencies, which are priced with reference to it rather than gold, are to a greater or lesser extent in the same boat.

Taking a cue from our analysis of the workings of cross-border monetary flows, which allows America to have its privilege of foreigners financing its deficits, we can estimate the approximate extent of the accumulated imbalances that could lead to the dollar's collapse.

We know that the US balance of payments deteriorated from 1992 onwards, though those figures did not include military spending abroad, which has been a significant and unrecorded addition to dollars both in cash circulation outside America, and also to estimates of the balance of payments.[vi] Official balance of payments figures are therefore understated and have been for at least a quarter of a century.

More recently, from September 2008 the Fed began expanding its balance sheet by policies designed to increase commercial bank reserves, as a response to the financial crisis. That August, they were $10.5bn, increased to $67.5bn the following month, and peaked at $2,786.9bn in August 2014, since when there has been a modest decline. From our analysis of the run-ups to the two previous dollar crises, we know we should try to estimate how much of the increase was effectively funded from abroad. Treasury TIC Data gives us a fairly good steer to what extent this has happened. We find that between those dates, (August 2008 – August 4014) foreign ownership of dollars increased by $6,237.7bn, over twice as much as the increase in the Fed's record of commercial bank reserves.

This is Triffin at its most fast and furious. Since then, foreign ownership of dollars has increased a further $2,142.4bn to a record $18,694.1, even though bank reserves declined by $572bn.[viii] In other words, the accumulation of dollars in foreign hands now stands at over 95% of US GDP.

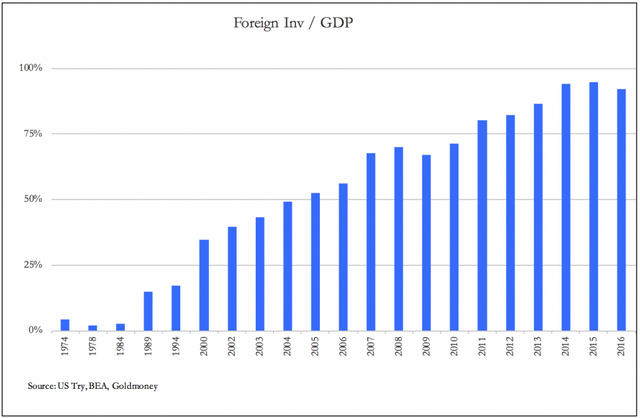

Another way of looking at it is to assess the market values of US securities held by foreigners and relate that to GDP, though this information is less timely,. This is shown in the following chart.

The build-up of foreign investment in America, in large measure the counterpart of dollar loans to foreigners, has been remarkable. At the time of the dot-com bubble, it had jumped to 35% of GDP, from less than 20% in the nineties and considerably less before. At over 90% of GDP in recent years, there can be no doubt that the next financial event, whether it be derived from a rise in interest rates or a general weakness in the dollar, can be expected to trigger a substantial flight out of the dollar.

The pricing of financial assets, and today's extraordinarily low interest rates indicate that a flight from the dollar is the last thing expected in financial markets. If they were still alive, de Gaulle and his economic advisor, Jacques Rueff, would be instructing the ECB, as successor to the Bank of France, to dump all dollars for gold immediately. And probably to dump all other foreign fiat currencies for gold as well. However, today, it is likely that other actors will blow the whistle on the dollar, such as the Chinese, and the Russians.

For it is clear that when the over-valuation of the dollar is corrected, the downside of a dollar collapse is far greater than it was in the early-thirties or the early-seventies. All other fiat currencies take their value from the dollar, not gold. So, the destabilising forces on the dollar, the other unexpected side of Triffin's dilemma, could take down the whole fiat complex as well.

Non-adapted content found at zerohedge.com: Source

gold silver and crypto!

This is the monetary crisis of the modern century, I hope in a short time will be better.

Nice post and agree. I have 2 targets at this time.

Price will never see $100 again.

Nice post, thanks for sharing

the dollar will remain valued as long as it is the defacto currency for oil the world over. The time that stops happening, the world dominance of the US dollar will erode - and the US will do everything in its power to ensur ethat doesnt happen

We really have to get more and more coins because our ugandan sh ugx is not going to collaps too badly.

Now i know the reason why many people are saying that dollar might continue depreciate in value as i red through your post .thanks for this informative and educative post.

Cool post, Thank you!

To listen to the audio version of this article click on the play image.

Brought to you by @tts. If you find it useful please consider upvote this reply.

Gold has always been a solution that is supposed to be more stable (less volatile) than all the others financial assets. But we are living moments without precedent with so much technology being introduced in our daily lives in the last 30 years.

I believe that history repeats itself, especially in the markets, so I completely agree with the fact that value of dollar will go down for the third time in history.