Cryptocurrencies - a new asset class

This is the content of a presentation I did on March 15, 2022, hosted (online) by UBI (United Business Institutes, a private busienss school with campuses in Bruxelles, Luxembourg and Shanghai)

The aim of this presentation is to introduce cryptocurrencies to a non-technical public with interest in money, finance and investing.

I'll start therefore by "setting the scene" with a little vocabulary: whoever is interested in finance is expected to understand notions such as "financial asset" and "portfolio management".

Financial assets and portfolio management

A financial asset can be ascribed a monetary value, it generally displays high fungibility, it can be transacted and it might have a duration. The set of financial assets of an investor constitute her "portfolio" and "managing" it consists in decisions, taken at specific moments in time, to convert (through "transactions") certain assets in her portfolio into other assets, with the objective of maximizing the aggregate monetary value of the portfolio.

Among financial assets one can distinguish various "classes", such as "cash", "real estate", "securities", "currencies", "commodities", etc.

When we talk about portfolio management and investing, discussions are usually framed by three questions:

- the "Why?" - i.e. strategy - why deciding for "this" rather than "that"

- the "What?" - the range of available choices

- the "How?" - the very important execution specifics

Cryptocurrencies enter the financial landscape

In the last 4 - 5 years, more and more financial analysts, such as Bloomberg and those of US banking giant JP Morgan have come to elevate cryptocurrencies to the status of a new asset class. This is remarkable in more than one way.

First of all, new asset classes are not appearing frequently, if at all: prior to "cryptocurrencies", it's hard to recall when another "asset class" appeared for the last time.

Secondly, cryptocurrencies are fundamentally a technological creation. Technological innovation has been running at dizzying speed for several decades and its impact has pervaded almost all walks of life. The financial industry has seen its operations deeply transformed already. Through cryptocurrencies, technology is now expanding the very substance on which finance operates.

Money

One of the first observations when analyzing the emergence of cryptocurrency as a new financial asset class is that it invites us to reasses money, the concept at the center of finance.

A concept we al think we understand but which is actually much deeper than we believe.

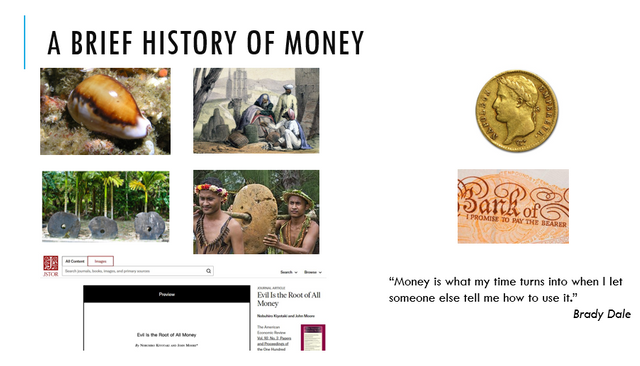

A brief history of money

I had reflected in previous posts, such as Blockchain revolution: Money and credit, on how the meaning of "money" has evolved in history

I would like to remind here that the three main functions of "money":

- unit of account

- medium of exchange

- store of value

were fulfiled at various times and places in human history by salt, cowrie shells or big discs carved out of granite (the Yap stones) before this wounderful invention was refined as precious metal coins emblazoned with a "trust figure" - "the king" or "the emperor".

Two axes of evolution can be observed here: the support / substrate or "container", and the actual "content", which is abstract and turns out to be "shared social convention" and "trust". In modern times, we gradually shifted the focus away from the container and toward the trust dimension of money, as the support became flimsy, worthless paper printed with a source of high trust (like the British pounds bank note in the image above, carrying the signature of the Bank of England as well as -not shown- the image of the Queen).

This led to new theories such as the "credit theory of money" - money as an "acknowledgement of debt", an IOU. Papers such as "Evil is the root of all money" by N. Kiyotaki and J. Moore analyse how the need to have this "IOU-type" money circulate led to the centralization of the emmission function in specialized institutions, the banks.

At a more personal level, an useful definition of money is proposed by CoinDesk's Brady Dale:

Money is what my time turns into when I let someone else tell me how to use it

Brady Dale

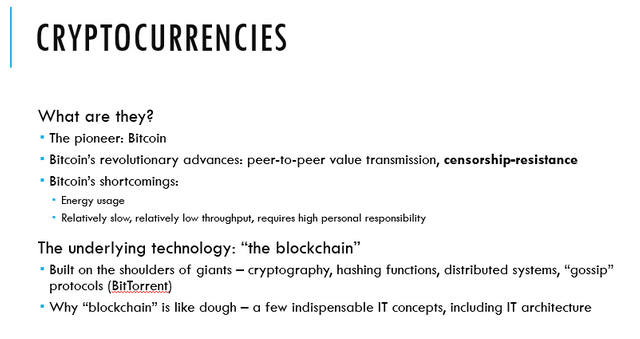

A short introduction to "cryptocurrencies"

By now, it's hard not to have heard about the precursor, Bitcoin. Bitcoin revolutionary advances included

- peer-to-peer value transmission solving the "double spending" problem

- censorship resistance

Indeed, the difficulty of using "data" as a substrate and "container" for "money" stems from the ability of data to be replicated at no cost. If we look at money as a "promise of time" (which is unique and cannot be replicated), it appears that something needs to be put in place in order for "money" to be represented by a "data object" (rather than a "paper object" or a "precious metal object").

Today's financial industry uses complex IT systems, processes and institutions to ensure that "data money" is as unique as time and cannot be easily replicated.

In contrast, bitcoin combines existing technology such as cryptography, hashing functions, distributed systems, etc. in novel ways in order to create a data object that behaves like money from inception, without the need of special-purpose processes and institutions. The design pattern its (pseudonymous) creator Satoshi Nakamoto has used is since known as "the blockchain".

"Censorship-resistance" has been observed to be another remarkable feature of the bitcoin design. As it happens, the power to create money is guarded jealously by those who possess it. Several previous attempts into prying open this monopoly were met with the full force of the law, censored, and their promoters put in prison. Bitcoin's creator was aware of their fate and thought carefully in order to create a resilient design, which is almost immune to the law, and thus resistant to censorship.

Bitcoin's shortcomings include its energy usage and the fact that its transfers are relatively slow, have a rather low throughput and require high personal responsibility as they cannot be rolled back.

I discussed the "energy issue" in several previous articles, including "Blockchain and the environmental challenge" (here is an english translation of my original French text) and "Bitcoin, soldier of reason".

From bitcoin to ten thousand cryptocurrencies

"The blockchain" pattern allows teams with technical know-how to create a new cryptocurrency.

"Blockchain" is like dough: it can be shaped and modelled in countless ways. Change a tiny parameter here or there, or replace almost everything keeping only the strict minimum - no one will sue for a "misappropriation" of the label "blockchain" or "cryptocurrency".

Today's financial industry uses complex IT systems, processes and institutions to ensure that "data money" is as unique as time and cannot be easily replicated.

The "Why?"

There are, of course, many "why"-s that can be asked. I've picked three:

- why are there so many cryptocurrencies, what differentiate them?

- why did they spawn a new asset class?

- why invest in them?

We mentioned above that, given the open source, free nature of the bitcoin code, skilled teams can spawn a new cryptocurrency relatively easily. But aside from the fact that "it's possible" and "it's not too costly", what else justifies the "cambrian explosion" of cryptocurrencies we've seen in the past 10 years ?

First, it is important to consider two aspects:

- narrative, and

- community.

Indeed, cryptocurrencies are inseparable from "stories", narratives, manifestos of some sort, stating the aim and purpose of each one of them. Most often these stories are told in a "whitepaper". Depending on how convincing the whitepaper is, a more-or-less large community acquires that cryptocurrency (usually buying it with another cryptocurrency) and either tries to contribute something to advancing the "vision" of the whitepaper or, more often, simply waits for the value of the new cryptocurrency to increase.

Second, we need to distinguish between two different types of cryptocurrencies:

- coins

- tokens

"Coins", like bitcoin, ether, litecoin or even dogecoin are the native assets of an autonomous blockchain system.

However, the second most popular blockchain, Ethereum, introduced a revolutionary functionality: it bundled a "code execution engine" (called EVM or "ethereum virtual machine") with the blockchain database. All of a sudden, the users of such a system had not only an immutable database, but also the ability to instruct the ethereum blockchain to execute user-generated computer code, programs of their own making. This proved wildly popular, not less so because of the catchy name such programs got: "smart contracts". Ethereum became the epitome of "blockchain" and inspired a large number of copycats.

Among the most popular such "smart contracts", deployed initially on Ethereum but now pervasive on all the Ethereum-"look alike" blockchains are those which create ... IOUs: they allow a user of the blockchain to convert some of her "ether" coins into ad-hoc financial assets which are transactable (can be sent from an address to another), can be fungible (or not) and usually have infinte duration.

These IOUs are the "tokens" living on the ethereum blockchain, but there are nowadays smart contract-generated tokens living on many other blockchain systems.

It is much easier to create a new "token" on an existing blockchain than it is to launch a new blockchain system bearing a new "coin". That is why most cryptocurrencies listed today are tokens rather than coins.

The value of a token is expected to be more volatile than that of a coin. Because a coin requires a higher investment, its value is somewhat better protected downwards by the "sunken cost fallacy": once people have invested years of time, effort and money in running a blockchain "node", they are loath to abandon a project which couldn't quite achieve its stated objective. In contrast, launching a token is so easy, it can be viewed as an exercice in marketing.

Why "a new asset class"

First of all, it is immediately apparent that their substance is quite unlike any existing asset class. Most notably, from a legal standpoint, most cryptocurrencies have no counterparty. They are not, in a legal sense, financial contracts, because there's no legal entity on "the other side of the deal" which undertakes any responsibility as to the value or fitness for any purpose of these assets. Another way of putting it is: "they are not backed by anything".

And yet cryptocurrencies are transactable (and fungible) like many financial assets. Above all, and rather surprisingly for old hands from the financial industry, they have a monetary value. How did cryptocurrencies acquire monetary value and what does it rest on has been the topic of heated debates and still is.

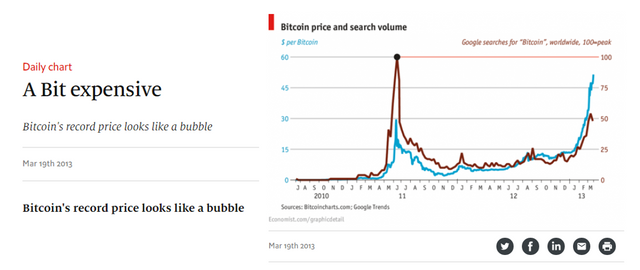

Many renowned economists (often old, privileged men) have kept repeating for more than 10 years that "Bitcoin has no fundamental value and its price will go to zero". During that decade, the price of Bitcoin underwent a 10 000 times appreciation, from about $4 - $6 in 2011 - 2012 to somewhere between $40 000 and $60 000 in the past year.

Yet another group of economists have tried to dismiss Bitcoin's price appreciation by comparing it to the Dutch tulip mania from the XVII-th century and referring to Kindleberger's classic "Manias, Panics, and Crashes". However, after four different "bubbles" which took its price ever higher, it became harder to offer the "tulip" explanation.

The price of Bitcoin underwent a first "bubble" in 2011 when, between February and December of that year, it went from $2 to $31 and back to $2. The image above (courtesy The Economist) illustrates that first top as well as the beginning of the second which saw the price of Bitcoin culminate around $1300 in November 2013

I offered an analysis into what underpins Bitcoin's value in a post from 2018 titled What's Bitcoin's Value?

The fact that there is, to date, no consensus on what confers value to cryptocurrencies is an additional argument in considering them "a separate asset class". It also illustrates the complexity of a phenomenon which has not only technological but also social dimensions.

Why invest in cryptocurrencies?

The last "why?" is the easiest to answer: because the higher risk is ... not investing in them!

Basically, cryptocurrencies are a very complex technological and social phenomenon. It's hard for anyone to claim to understand them fully, let alone to be able to predict how they will behave in the future.

People who dismissed Bitcoin as "Dutch tulips" during its bubbles of 2011 or 2013 are probably now regretting not having bought some, even at the tops of those bubbles. This is why I advise humility and rationality. Indeed, in a 2017 article I argue that Not buying Bitcoin is irrational.

My assumption is one which has been proved right time and again, by the fall of the communist regimes and again by the success of cryptocurrencies: "People respond to incentives".

Applied to me and you, it follows that investing a small, reasonable amount of money in cryptocurrencies offers an incentive to learn more about them, it gives one the proverbial "skin in the game". If you use an investment in cryptoassets as an additional reason to study and learn about them, then you cannot lose, whatever trajectory their value takes: if it's "up", you win; if it's "down", you would have learned a valuable lesson.

Consequently, by not investing in cryptocurrency you deny yourself the possibility of a financial gain and an additional lever of motivation to study and understand a hard, complex yet promising field.

The "What?"

Once we agree on the "why?", the "what?" becomes a matter of detail. The main question is probably "what cryptocurrencies to invest in?"

As an investor, one needs to consider the contribution to the performance of their portfolio of two main factors:

- asset price appreciation

- asset-generated income

In order to optimize the former, one needs to transact more often, converting more sluggish assets into faster-appreciating ones (and hoping the trend does not reverse). This is usually called "trading" and bears several hidden costs. The most obvious, but not the highest, is that incurred from "transaction fees". However, a much higher cost comes from the time and effort needed to research, devise and execute the right sequence of transactions at the right moments. Probably the highest cost is that of the risk taken of swapping into the wrong coins or at the wrong moment (or both).

It is therefore fortunate that the industry is very young and its overall size keeps growing. As the proverb says, "a rising tide lifts all boats". That is why it might not be absurd to imagine purchasing a few cryptocurrencies one has researched and has confidence in, and then simply waiting to benefit from being among the early adopters.

On the other hand, generating income from one's holding of cryptoassets is somewhat more "involved", albeit becoming easier every year. Here we mention both "interest bearing products" of the centralized exhanges and the newfangled "DeFi" (decentralized finance).

A serious treatment of these topics cannot be done in the space of a short presentation and is left as an exercise for the reader. A word about volatility is warranted though. As I said, this is a new, complex, little understood asset class. People investing in it are like pioneers with a relatively high risk tolerance, but very quick to react even to little understood signals. A lot of investing is driven by "momentum" or "sentiment". Hence we see a lot of correlation between the various cryptocurrencies. This amplifies both downward and upward price movements. What in the world of stocks would be a sign of a "major crisis", in the cryptocurrency world it is a "normal daily range".

The "How?"

Going into more detail, the next question is quite practical: if one were to invest, how would one start?

At first, the only way to acquire cryptocurrencies was "working to get them" in a process called "mining". As the "cryptocurrency mining" activity sought a higher efficiency and economies of scale, it became an industrial pursuit. With a few notable exceptions, it is now all but impossible for an amateur to be able to join in "mining" (thus earning cryptocurrencies in exchange of labour) without also laying out a significant amount of capital.

Subsequently, exchanging money for (i.e. buying) cryptocurrencies became the normal route. At first there were a few sites which facilitated peer-to-peer physical exchanges, like LocalBitcoins.com. Then, cryptocurrencies exchanges appeared and managed to establish a banking relationship. "Investing in cryptocurrencies" became a matter of creating an account on a "crypto-exchange", transferring money to it and then buying from there. I wrote a more detailed article a few years ago, called How to buy Bitcoin in the eurozone. A few things have changed since, but this article will still give you an overview of a possible path to follow.

In this context, it is important to observe that traditional banks act as "gatekeepers" and exercise a censoring power: they often have the regulators in their pockets and can decide, on the fallacious argument of "protecting investors", to sever a crypto-exchange connection to the traditional finance world, thus making it considerably more difficult and costly for people to use that exchange. This happened last year to Binance, one of the most versatile crypto-exchanges, which used to be connected to the network of SEPA transfers through a bank located in the UK. But the FCA (the British regulator) decided to "protect investors" and ordered the correspondent bank to stop serving Binance.

Other typical tropes used by the incumbent financial industry to defend their privileged position against the new crypto entrants are the sempiternal myths about "money laundering" and "illegal activities". That's why a little "mythbusting" is in order.

Mythbusting

We keep hearing both banks and financial regulators (who are often a lot less independent than they should) that "cryptocurrencies are aiding and abetting money laundering and illegal activities". The truth is a lot more nuanced. As a "value transfer chanel", a certain amount of money laundering and illicit activity is of course expected. However, there are structural arguments as to why this amount is, and always will be smaller than in the classical financial system.

As shown in the image above, the amounts laundered in the classical, opaque banking system are orders of magnitude bigger than on the bitcoin blockchain. Even in relative terms, there is less illicit activity on public blockchains, thanks to their transparency and immutability

- Complexity. The complexity and lack of familiarity of the cryptocurrency environment is the biggest deterrent for money launderers and other criminals (with the exception of cybercriminals). These unpleasant characters have been doing their business for years through the classical banking system and unless there are compelling reasons, they are understandably reluctant to risk their ill-gotten gains in a new, hard to understand and, unlike corruptible bank employees, impossible to control environment.

- Lack of liquidity. Small scale money laundering can and usually is done in cash. For the big sums, most cryptocurrencies simply do not offer enough transactional volumes to effectively hide big sums. This argument is to be read in conjunction with the next one.

- Transparency and immutability. All the blockchain transactions (with the exception of a few "privacy" coins which have very little volume) are transparent and visible to all. Even though they are conducted between "addresses" and not between individuals, transparency allows thorough data analysis which can uncover tell-tale patterns and have led in the past to capturing the criminals. The European regulators are often considering that blockchain addresses do not offer individual data protection up to the standard required by the GDPR - precisely because it is sometimes possible (albeit difficult) to identify a person by combining information including its pseudonymous blockchain activity. Moreover, blockchain transactions remain forever visible. Even if at the moment of the illegal activity there is not sufficient information to link an address to an individual, subsequent activity and transactions might in the future allow law-enforcement to work their way to the criminal simply because the traces it left on a public blockchain can never be erased.

Therefore, any aspiring money launderer or criminal worth his salt would rather bribe a bank clerk who can, if push comes to shove, destroy incriminating documents, than risk a forever-visible and never-erasable blockchain transaction which might inadevertently lead to him even a decade later.

Looking forward

Time to wrap-up and consider the "take aways" of this presentation:

- Cryptocurrencies are a new asset class whose relevance has only been increasing for several years. It's worth recalling here that publicly listed companies such as Tesla and MicroStrategy have added Bitcoin to their treasury, and that El Salvador has recognized Bitcoin as "legal tender". Digital scarcity (there will never be more than 21 million bitcoins) implies timing matters.

- Because of their complexity and novelty, their market behaviour tells more about the moods of the investors than about underlying fundamentals.

- Their extreme volatility also reflects a relatively shallow market, easy to move by relatively low volumes.

- When pondering the price drivers, one should look at the narrative, at adoption and only later at the innovation brought by a coin or a token. However, there's little to no downside for promoters to making misleading or downright fraudulent claims, so "buyer beware!"

Final word

There's no reason not to try. You never lose: you either win, or you learn