Two Sides of Free Money on Compound.Finance - and Opportunities for Staked.us

Introduction

DeFi or Decentralized Finance is changing the ways people interact with money. Check this CoinTelegraph article on ‘decentralized finance, explained.’ DeFi empowers people across borders to bank in ways that only the underlying trustless, immutable tech that is Blockchain could allow.

In this article, we’ll look at two new and novel ways to approach lending and borrowing to achieve previously unheard of situations. Traditional lenders and institutions would cringe if they knew more people were aware of how to use their funds wisely. We can both avoid unnecessary fees and middlemen by using DeFi.

The difference among DeFi and centralized finance is that with DeFi you hold your keys and nobody else has access to your funds - only your wallet, interacting directly with the platform or protocol. There’s no middlemen and no counter-party risk. You can read more about the risks involved with handing over your cash to a middleman in this other article I wrote.

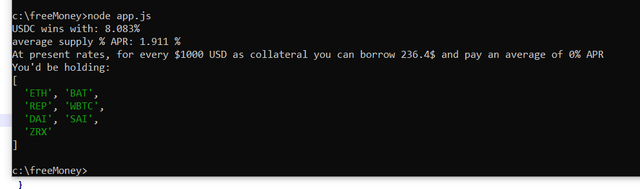

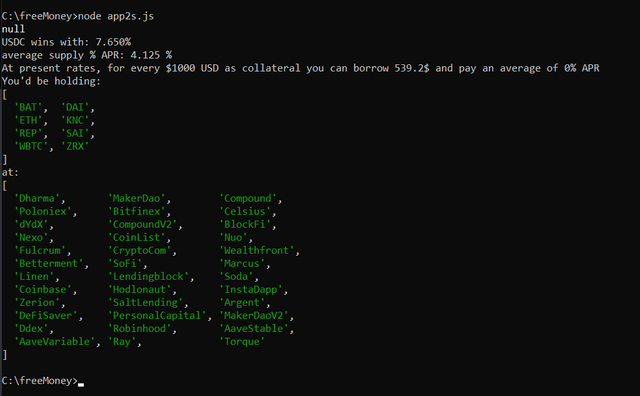

Free Money #1: 0% APR Secured Loans

I coded a small script that checks the borrow and lend rates on compound.finance. I then calculated which of the coins backed by USD (stablecoins) I could borrow for the least amount of annually compounding interest. Next, I got the average of lending interest rates for all the other coins on the platform. Dividing the two into a quotient, I can get an amount I can borrow as a secured loan against my capital - while lending to an index of the other coins on the platform - to effect $0 per year in accrued interest on my loan.

If someone were to build a platform on top of this, they could include other DeFi solutions like torque.loans and fulcrum.trade to net even more beneficial rates of yield and interest on amounts borrowed - meaning you could index more coins and generate a higher $0 and 0% borrowing amount. The platform would show your gains/losses for the tokens on next login - and there’s a chance your BTC or ETH (or any other token) have appreciated 10x since your last login, allowing you to borrow more at $0 or 0%. During that time, your holdings would have appreciated based on the difference of lend/borrow rates. In the case some tokens depreciate in face value, your interface would present you with a ‘rebalance’ option. It would allow you to deposit (and then index) more to all the tokens or whichever you’re most comfortable with. If you decide to lend DAI and borrow USDC, another interesting idea pops up…

If you have equity and want a cotterilizied, on-chain solution to it, you can borrow risk-free by doing 0% loans.That would bring a bunch of interesting endeavors. I do have some friends that would pounce on capital secure, fully liquid (withdraw your capital at any time, less the fees into locked, secured accounts that you can trust- trustlesly.

Look, more DeFi is more eggs in more baskets (in a risk-averse sense), and even finds more competitive rates to use against USDC so you can have more than half your money back while hodling a cross-selection of Eth and Ether tokens (like Wrapped Bitcoin) that might potentially explode in value.

We can index and figure out which are non-custodial, then launch a service.

Free Money #2: Interest Rate Arbitrage: Borrow to Yield

Now, 0.73% difference doesn’t sound like much. Let’s keep in mind that a new platform with a new smartcontract might for instance copy what staked.us does for RAY contract and get even higher yields by indexing more DeFis, where the yields are sometimes higher. For the purpose of this doc we’ll say the solution in place uses compound’s smart contracts. I’d already figured out the web3 magic in the past to deposit and withdraw from compound.. This means our funds will remain liquide and we can ‘double down’ our proceeds in the same interface.

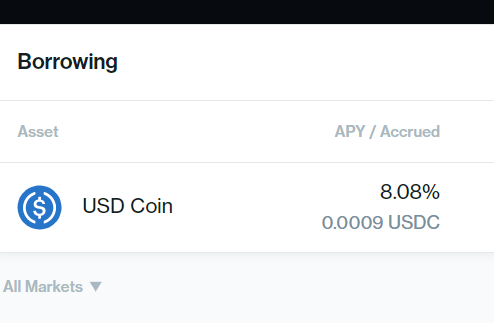

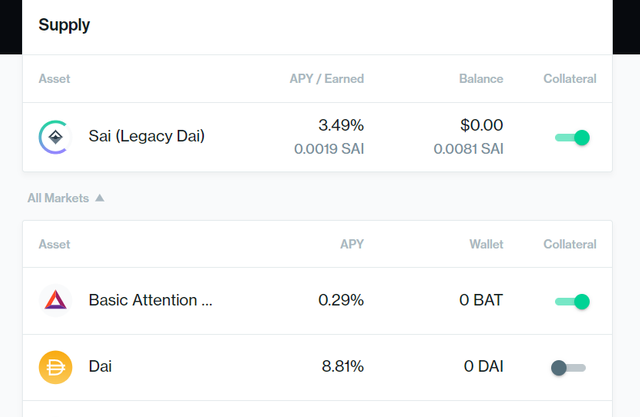

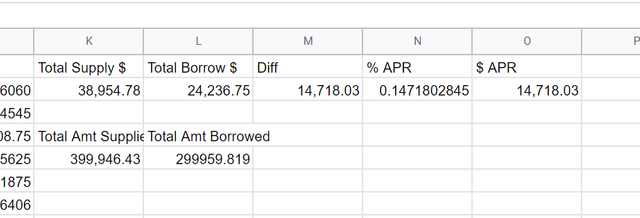

Now, on Compound we can deposit anything and get our capital out without a lockup. If I lean on Compound I still earn interest on the asset I borrow. I start off with $100 000, and I can get $75 000 USDC by completing that loan. Now, I’m paying 8.08% APR on the $75 000. My portfolio size is now $175 000. Now, I repeat. First, I go to uniswap and transfer USDC for DAI. I take the maximum loan I can from $75 000, and I can increase my portfolio size to $400 000. It’ll look something like this:

Remember that you can only ‘bite off more than you can chew’ in situations like these, where you earn more from lending another like asset (meaning the value would be or remain around the same).

Now, it’s important to think that if you’re risk-averse to speculative to coins rises or sudden falls, it’s possible to exclude the speculative coins from the list of coins they’re considering - say, only hold DAI and SAI, never Eth or WBTC.

Conclusion

I’m daring the fine folks at staked.us to build these into fully functionable marketable products - or by streamlessly linking them to their current Robo Advisor for Ray, have a look:

https://github.com/Stakedllc/robo-advisor-yield/issues/11

https://github.com/Stakedllc/robo-advisor-yield/issues/12

EDIT: Turns out Great Minds Think Alike (or Simple Ones Seldom Differ): https://github.com/Stakedllc/YIPs/issues/8