CoinDesk Releases Q1 2018 State of Blockchain Report

After reaching historic highs in 2017, cryptocurrencies languished across multiple fundamental metrics in this year's first quarter.

Unease permeated the industry, mostly from regulatory uncertainty and pull-back after a year of parabolic growth.

To shed light on a tumultuous Q1, CoinDesk's latest State of Blockchain report provides a 90-plus slide analysis of some of the most significant data points.

Released Monday, the report covers public blockchains, distributed ledger technology (DLT), consortium chains, initial coin offerings (ICOs), trading and investments, and regulation. It also features the results of our 50-plus question sentiment survey, which provides insight from over 420 CoinDesk readers.

Here are six of the most important trends that defined Q1 2018:

- Bear market for crypto

Following an all-time high of nearly $20,000 in the previous quarter, bitcoin suffered a 51% decline in Q1. Other fundamental metrics, such as transaction volume, transaction count, and exchange volume, saw similar drops.

Most altcoins mirrored this behavior and followed bitcoin down, with correlation coefficients of returns ranging from 0.7 to 0.9. The entire cryptocurrency market capitalization lost about $348 billion.

The numbers may look grim, but that didn't show up in overall sentiment: 79 percent of the respondents to our CoinDesk Sentiment Survey thought this bear market would be short-lived.

Eighty-six percent said this was a correction after the rampant over-speculation of the prior quarter while 62 percent said that regulation was a depressing factor.

- Market matures

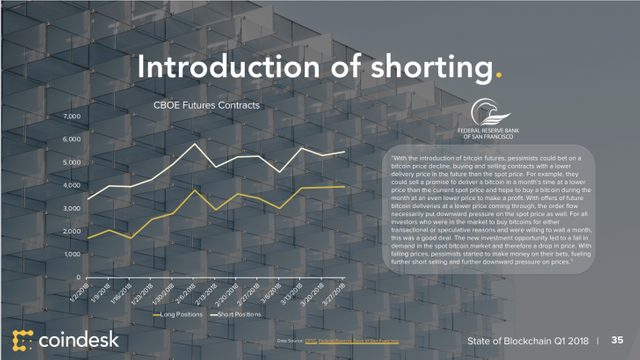

After the introduction of bitcoin futures markets at the end of Q4, we've seen steady growth in this activity through Q1. Both long and short positions grew - but strikingly, the shorts outnumbered the longs.

Short positions ended the quarter at about 5,000 and long positions ended at about 3,000. It appears that it's mostly pessimistic investors taking advantage of these contracts.

And this, in turn, appears to have contributed to the slump in the underlying asset.

According to researchers at the Federal Reserve Bank of San Francisco, "the new investment opportunity led to a fall in demand in the spot bitcoin market and therefore a drop in price."

- Miners stay long

Bitcoin miners didn't appear phased by the dips, however.

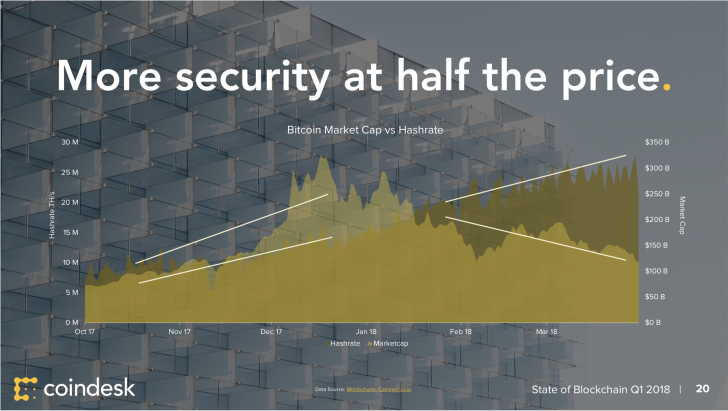

Over Q1 we saw the slope of hash rate - the amount of processing power devoted to securing the bitcoin network - diverge from market cap, instead of each moving in the same direction, as in Q4 2017. The hash rate grew 47% over the quarter with little deviation.

Bitcoin's hash rate held strong against the competition; bitcoin cash, the cryptocurrency with the second-strongest hash rate, averaged only 12 percent of bitcoin's hash rate over the quarter.

It's also important to note that miners tend to take a long-term view and offer a counterpoint to short-term pessimists. Seven percent of our respondents said they learned more about miner dynamics during Q1.

- Taxes loom large

Taxes were top-of-mind for many investors, with cryptocurrencies generating an estimated $70 billion in global tax revenue for 2017, based on the total gains in the market and the average of various governments' tax rates.

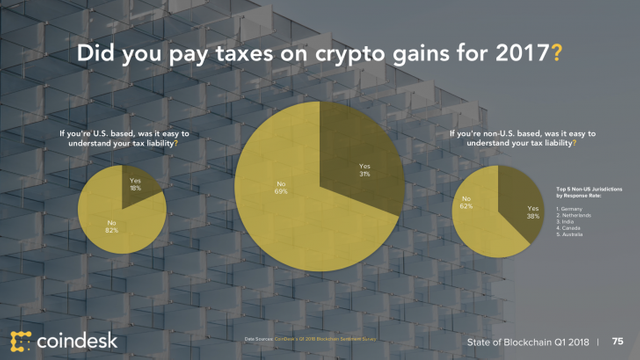

The tax parameters surrounding cryptocurrencies remain in flux. Thirty-one percent of survey respondents said they paid taxes on gains; however, the number of those obligated to pay taxes might be higher than those that report taxable gains.

Of U.S.-based respondents, 82 percent indicated that it wasn't easy to understand their tax liability while 62 percent of non-U.S. based respondents said the same. These observations lend support to the theory that people (regulators included) are genuinely confused about the legal and tax status of the entire asset class.

The 20 percentage point difference in tax understanding between the U.S. and non-U.S. respondents could indicate the U.S. is failing to embrace the next generation of financial technology as competing countries consider friendlier strategies.

- ICO growth continues

ICO activity remained brisk, with $6.3 billion raised in Q1. Monthly breakdowns of ICO raises show each individual month of Q1 was higher than the record amount set in December.

Telegram's $1.7 billion ICO was a large outlier that accounted for over 25% of the funding in Q1. The next-largest ICO in this period was Dragon's $320 million offering. Without Telegram, the tally for March would have been below December's.

Yet larger ICO raises appear to be a growing trend. The average raise amount almost doubled from Q4 to Q1, from $16 million to $31 million. The distribution of ICOs shifted towards larger raise amounts and fewer total deals.

The number of ICOs declined each month from December's high of 78, except for a slight uptick in March. While the reduction in the number of ICOs might seem like a bearish signal, 40% of survey respondents participated in an ICO, up from 30% last quarter.

- Fees fall

Transaction fees on the bitcoin network dropped from drastic highs set by the feverish demand of Q4 2017, when on some days fees averaged $40. Over Q1, fees settled on an average of $9.49 per transaction.

Most other cryptocurrencies saw 60 to 90 percent declines in fees as well, but in absolute numbers, they were never so high prior to Q1.

High fees might have discouraged users from transacting, but it's unusual to see fees come down and still see declines in transaction counts. Fee levels are also a barometer of demand. As more people bought into cryptocurrencies in Q4, we saw increases in fees. So a reduction in fees could imply that demand is shrinking.

There are solutions to help mitigate fees further, most notably the lightning network, which made important strides in the first quarter and shows promise as a stable, second-layer solution for frequent and smaller transactions.

Seventy-eight percent of our respondents considered lightning a positive development and look forward to using it. And while 21 percent suggest lightning will centralize bitcoin more, the other 79 percent think there will be no change or less centralization because of it.