Blockchain for Business #1: What is a blockchain?

Business networks are often inefficient because each participant in the network keeps records of all transactions between all the parties that the business interacts with. This process causes the duplication of common information and multiplies the costs of mantaining these data.

One solution to this problem could be to use a blockchain, which provides a shared ledger technology. This allows any participant in the network to access the common records in a single place: a shared ledger.

What is a blockchain?

A blockchain is a peer-to-peer distributed ledger, forged by consensus, combined with a system for smart contracts and other assistive technologies.

Blockchain can be useful in order to build a new generation of applications. Since it provides trust, accountability, and transparency. In addition, it lets taking into account also business processes and legal constraints.

Blockchain structure

Every blockchain has the following structure:

- Genesis block: initial block. More generally in distributed ledger we talk about initial record.

- Each block includes one or more transactions

- Users can connect to blockchain using a specific application (i.e. a wallet)

- It is possible to transfer digital assets (i.e. cryptocurrency) from one user to another. This operation will move some asset from one's wallet to another. The corresponding transaction is saved on a blockchain.

- Every new block is spread across the network and the syncing is based on consensus, an agreement between network peers.

Bitcoin: the first blockchain application

Bitcoin blockchain is the most well known and it exists since 2009. Blockchain is not Bitcoin or vice versa. In fact, a blockchain is a distribute ledger that can track various assets other than cryptocurrencies.In the Bitcoin blockchain, the miners collect unconfirmed and valid transactions into blocks. Miners must solve a cryptographic challenge to gain the right to insert the following block. This process is known as proof of work, and requires significant computing power.

Timestamping with blockchain

Timestamping is another key feature of blockchain technology. Each block has a timestamp. And every block refers to the previous one. Together with cryptographic hashes, this chain of timestamped blocks provides an immutable record of all network transactions, from the genesis block.

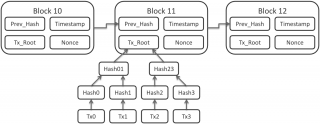

Blockchain blocks

A block commonly consists of four pieces of metadata:

- reference to the previous block

- piece of data (nonce) that let the miner won the proof of work competition.

- timestamp

- Merkle tree root for the transactions in this block

Difference between distributed ledger and blockchain

The concepts of blockchain and distributed ledger are not the same, in fact:- distributed ledgers are a new kind of decentralized database. So that everyone have a copy of ledgers transactions. Every transaction reaches the ledger owners in real time through synchronization.

- blockchain is a full set of new technologies. It includes DLT and even smart contract functionalities. It builds a chronological chain of blocks.

Blockchain properties and use cases

Finally let's see which are the main blockchain properties and its possible applications:- able to create distributed consensus between mutually distrustful parties

- allows us to create an instantaneous single source of truth (i.e bank ledgers, inventory systems, sales and deliveries,…).

- With blockchain we can record things in real time and we could even stop to launch night batch to process daily data. Instead, we're doing validation in real time, and we always know the current state. So, blockchain applies to manufacturing when it is possible to check the replenishment need and provide missing sources a few minutes before they run out. Or can apply to every other process where it is necessary to track materials, effort, money and so on.

- From a security perspective, blockchains are not going to improve our current business logic. They are more logging systems. In fact, when we talk about private blockchains, they’re permissioned networks, typically behind a firewall. When there are multiple organizations participating to the network there will be some tunneling technology and VPN firewalls to make a virtual LAN exist.

Hello, you received a boost courtesy of @steemdunk! Steem Dunk is an automated curation platform that is easy and free for use by everyone. Need an instant boost? Send 0.200 SBD with your full post url as the memo to @steemdunk for an upvote. Join us at https://steemdunk.xyz

Upvote this comment to support the bot and increase your future rewards!