Your ultimate guide to the upcoming fork that’s splitting the Bitcoin community

There’s a lot of fuss in the bitcoin community about what will happen on August 1. Will the cryptocurrency split into two new ones? Will it not? What is BIP 91? What is BIP 148? What is SegWit?

The incredibly significant date is just around the corner but there are still so many unanswered questions!

I have put together this guide to walk you through the whole situation to keep you informed about the developments. As of this writing, it seems like, bitcoin will avoid the chain split — for now. However, even though it seems like the opposing parties have reached a joint conclusion, there’s still a lot that needs to happen to avert the split.

To understand what’s actually happening and why the bitcoin community has split into two, it’s best to take a look at one of the fundamental issues of cryptocurrency — or to be more exact — how people disagree about how to fix that issue.

On one side, there are the people who manage the open sourced software for bitcoin. They are like the organisation/community that keeps the development on the bitcoin protocol running. On the other side are the miners, who deploy computers to run the bitcoin network (blockchain). Both sides are crucial to keep the bitcoin running — one side can’t do it without the other. And to fully understand the issue, you need to understand the mechanics of bitcoin, and that’s why I’ve tried to explain the complete deal with bitcoin chain split in this guide.

What is the problem with bitcoin?

Most people think of bitcoin as a digital currency that you can use to buy and sell things online. That’s technically correct, but that’s not bitcoin’s real value.

Bitcoins aren’t really feasible for everyday transactions, and we’re nowhere near being able to walk into a Starbucks and pay for our coffee in bitcoins. But why is that? Wouldn’t make sense for the makers of bitcoin to implement it as an real alternative to other currency, and thereby increase the value of bitcoin?

Well, the reason that hasn’t happened is that the bitcoin blockchain is slow and expensive. It’s nowhere close to meeting the standards for payment technology as the bitcoin network can process up to six transactions per second, while the VISA network can process over 1600 transactions per second.

The only way the general public will adopt to the decentralized network is if it will be as fast and convenient as existing payment networks. Unless that happens, bitcoin will be used mostly as an instrument to store value.

Why is the network so slow?

Bitcoin’s network is built on top of a blockchain. If you haven’t yet read the ultimate guide to understanding blockchain, think of blockchain as a register containing several pages (blocks) where each page contains several transactions. As soon as a page has been filled with transactions, it needs to be added to the register before starting to record transactions on the next page.

Before a page (block) can be added to the register (chain), there’s some processing that needs to be done to ensure that everyone agrees with the contents it contains. The process approximately takes 10 minutes for each block.

Imagine, you are sending 1 BTC to your friend, Joe. The transaction will look something like this.

![]()

Among other things, a transaction contains information about the sender, the recipient, the amount and the transaction fee.

Wait a minute, transaction fee? Yes, there’s an additional fee that you can pay to incentivize miners to include your transaction in a block as soon as possible. There’s no set price and it’s entirely up to you how much you are willing to pay to speed up the process.

At any given moment, there are several transactions available to be recorded on the current page. If you look for number of unconfirmed (pending) transactions any time through the day, the number will always be close to ten thousand. That’s when the 99 percent of the world is yet to come to cryptocurrencies. The number then can easily be north of several millions.

![]()

The miners (computers working in the blockchain network) have to decide which of the available transactions to include in the current block. To help them decide, they look at which transactions yield the most rewards — meaning that the transactions with the highest transaction fee will be included first.

![]()

If there are enough transactions with higher transaction fee than yours to fill up the block, your transaction will have to wait in queue. The wait can last from a few minutes to a few hours. And sometimes, even days. The more you pay in transaction fee, the quicker your transaction is processed.

![]()

For the users, using Bitcoin has become slow and expensive. Not exactly what the ‘money of the internet’ should be like.

However, this has prompted smart people to ask an important question: “How can we scale the capacity of the bitcoin blockchain?”

The funny thing is that there were too many smart people asking that question. The people who are running Bitcoin (the people who are maintaining the open sourced code that runs on people’s computers) believe in one solution, while the miners (the people who run the code on their own computers) believe in another.

The solution proposed by the people running Bitcoin favors the users, while the solution proposed by the miners favors themselves (what a surprise!). It’s this disagreement that’s led to the confusion around August 1 and the potential split of the Bitcoin blockchain. We’ll come back on this topic later in the post; let’s understand the solutions first.

The solution that favors the users

What the people running Bitcoin came up with originated in how we store a transaction in a block. The solution was originally to remove the malleability of blocks, but it had a positive side effect: it increased the capacity of the blockchain too. To understand it better, we’ll need to understand how blocks look like.

The solution is known by several names on the internet, such as SegWit, BIP 148 and UASF (User Activated Soft Fork).

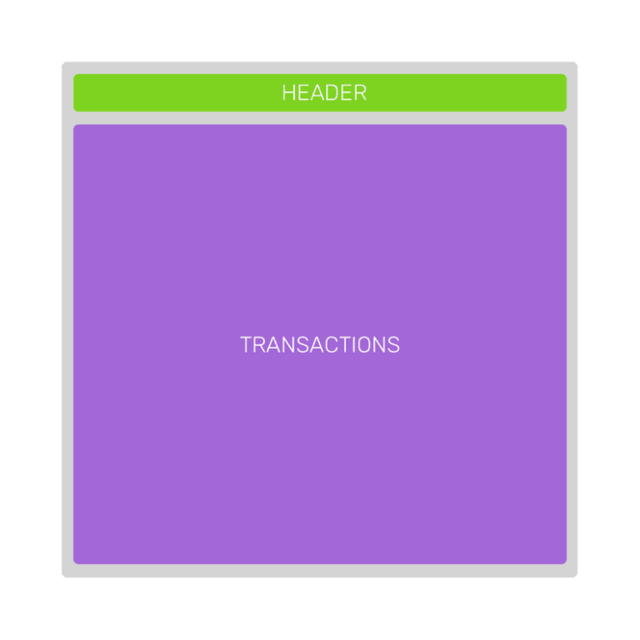

What does a block look like?

In the most simple view, a block in the chain has two kinds of data in it — header and transactions.

Header contains meta data of the block, but that’s not relevant to the August 1 fork. The header is tiny and only takes up about a percent of the block’s data. The other 99 percent of the block’s data is made up of transactions that are included in the block.

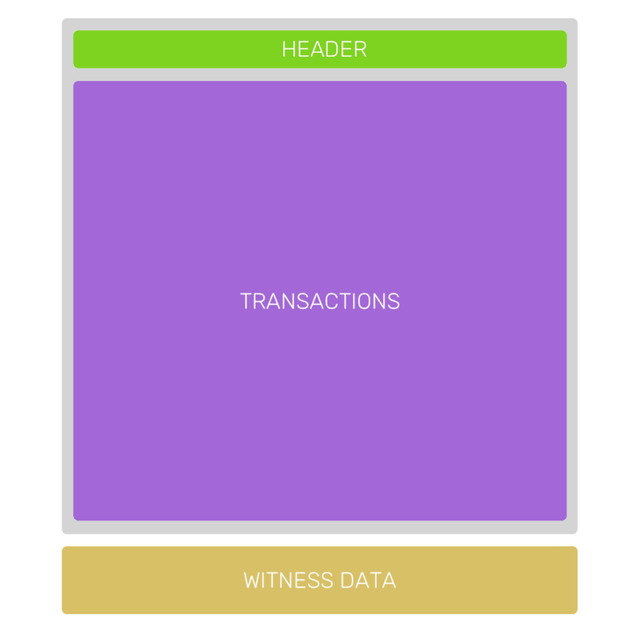

If we dig deeper to see what makes up a single transaction, we’ll find that besides the obvious things — like sender, recipients, amount and transaction fee — it also contains something called a ‘Signature’ or ‘Witness’. The Signature verifies that the sender has enough balance to send the said amount of bitcoins in the transactions. This particular data is only used once at the beginning, but it makes up almost 65 percent of the data in a transaction.

![]()

The total allowed size of a block is 1MB, and most of it is filled with data that isn’t critical to the block. The idea is to move the Signature/Witness data towards the end of the block in a separate structure.

This separate structure isn’t required to be included in the blockchain. If a node (individual participating computer in the network) can, it’s great. If it cannot, no big deal. Because of this property, it is called a Soft Fork.

Some nodes will update their software and begin working on the new block structure, while the nodes that decide to stay on the legacy software will simply ignore the Witness portion. This optimization in the structure allows more transactions to be included in a block.

This solution is technically called SegWit because of Segregating (separating) Witness from the block structure. And it favors the users.

How does SegWit favor the users?

The new structure can hold a lot more transactions than the current structure can. It causes the competition among unconfirmed transactions to be included in the block goes down. And with it, the transaction fee goes down. Transaction fees are a part of the reward that the miners get. With lower fee, the reward for mining the block will go down too. Not just that, this new structure also something that is called Lightning Network that allows micro payments (you paying for coffee at Starbucks) to be processed instantaneously without any fee.

The leading argument against this solution is that it’s a temporary fix and that a ‘Hard Fork’ will eventually be implemented down the road. And the Hard Fork is the miners’ proposition.

The solution that favors the miners

The miners propose a solution that will scale the network for a longer term. Their proposition is to implement SegWit (Soft Fork) like the users propose, and in addition to that, they also want to increase the size of the block from current 1MB to 2MB. Thus, the name — SegWit 2x.

Besides being known as SegWit 2x, the miners’ solution is also called MASF (Miner Activated Soft Fork) and BIP 91.

At first glance, this solution looks way better.

I can almost hear you shouting, “The network will be even faster. Yay!”

However, the devil lies in the details. If this solution is implemented, every miner in the network will have to upgrade their hardware and software. There is no concept of backward compatibility included in this solution. Those who won’t upgrade will be orphaned by the network. That’s why it is called a Hard Fork. Let’s take a closer look.

Imagine there are ten miners in the network, and that six of them decide to upgrade to larger sized blocks. These six will continue working on making the longest chain even longer, but their mined blocks will be discarded by the rest four who still consider old block size to be true.

How does SegWit 2x favor miners?

What do miners like? Higher rewards. What do miners like even more? Less competition.

Due to the fact that not everyone will have enough money to upgrade their computation power to mine larger blocks profitably, smaller miners will vanish away from the network. This will leave larger and fewer miners in the network — which dramatically reduces the competition.

When Satoshi Nakamoto presented the glorious idea of building a decentralized future, he didn’t mean it just in theory, but he meant it in practice. Putting power in the hands of few large miners goes against the foundational idea of bitcoin’s existence.

If you’d ask miners they’d probably say something like “We are running the network. We must have a say how we want to run it. If we shut our computers and go away, there’ll be no bitcoin.”

And if they did, they’d be right. But they’re also wrong.

They are right when they say there’ll be no bitcoin if they go away, yet they’re wrong because when they say only they are running the network, they’re saying it with the same intentions as that of people running regular banks and governments.

Blockchain is not just a software protocol that allows financial transactions. It is the protocol that changes the fundamental beliefs of our species.

With this protocol, there is no place for the sense of ownership. Everybody owns the network and nobody owns the network. The sooner we accept it, the sooner we’ll be able to make real progress.

What exactly is the split that everybody is talking about?

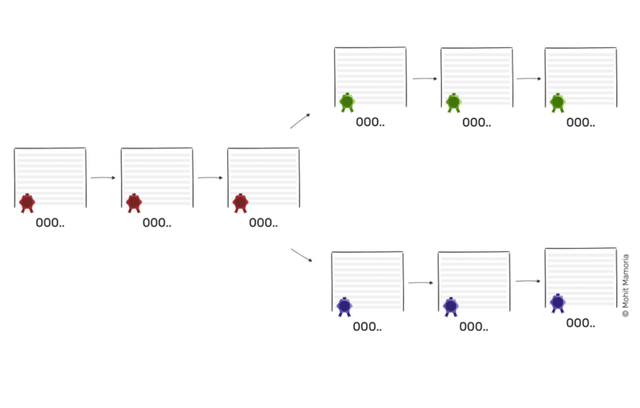

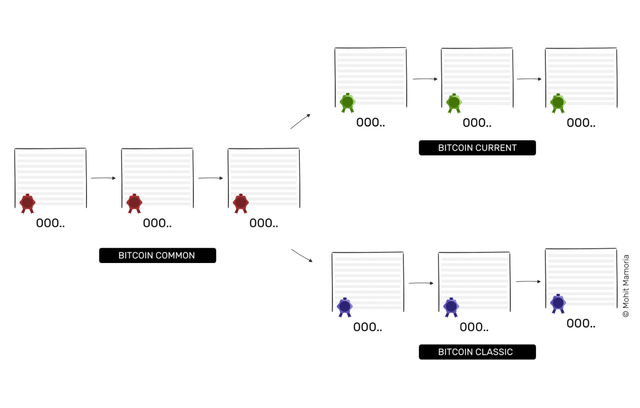

Remember when the blocks mined by six of our miners were discarded by the rest four? Let’s see what the blockchain looks like for them. The four miners who are working on the smaller block size, will continue mining their own set of blocks and will be making their own version of the longest chain.

When that happens, the blockchain will split in two blockchains. Some nodes will be working on one version and some on the other. Let’s label the resulting blockchain like so:

The ‘Bitcoin Common’ part of the chain is the part before the split. Miners with the upgraded computers will work on the ‘Bitcoin Current’ branch of the chain while the miners who are still on the old block size will form the ‘Bitcoin Classic’ branch of the chain.

Bitcoin, the currency, will therefore effectively be split into two. Coins that were collected by users during the Bitcoin Common can be spent on both Bitcoin Classic and Bitcoin Current. However, the coins that will be traded on Bitcoin Classic will be different from those traded on Bitcoin Current. They will be different in quantity, different in value and different in adoption. They will be as different as any two pre-existing cryptocurrencies can be.

What will happen to the bitcoins you own?

It depends where you’ve kept your bitcoins. If they are on your own computer, you can spend them twice — once on each blockchain. But if they are stored in an online wallet, the fate of your coins is in their hands.

Every online wallet will have their own take how they want to proceed with this blockchain split. They might either migrate your coins to one version of the blockchain or allow you to spend on both. It depends.

What I’d advise you to do is not make any transactions a few days before and after August 1, 2017. Because of the fork, you might lose your bitcoins into the thin air. After all, bitcoins are nothing but records of transactions. If you transaction doesn’t get recorded by either of the chains, they will be gone forever. Poof.

There’s a lot of turmoil around what might happen on August 1. Over last couple of weeks, markets have been more volatile than ever. As of this writing on July 24, 2017, almost all the miners are signaling BIP 91 (the miner’s proposition). With this, it seems like bitcoin will avoid the split on August 1, but it is not a guarantee still. Miners saying that they will implement BIP 91 doesn’t mean necessarily mean that they will. This is just a statement of intent from the miners.

To really implement BIP 91, majority of the miners will have to upgrade the software on all of their computer before August 1. Miners running the updated software is still under 50 percent.

If the miners stick to their intent over next week too, the SegWit part of SegWit 2x will be activated, and the 2x part (increasing the block size from 1MB to 2MB) will be on its way later this year, which will be a hard fork. What might happen during the hard fork? We’ll bring another guide then to keep you informed on the matter.

Thank you for clarifying about what will happen on august 1, advantages,disadvantages of these.

Your welcome

Thx for share