Lessons on Bubbles From Bitcoin Until there is a way to bet against an asset, its price will be set by the most upbeat buyer

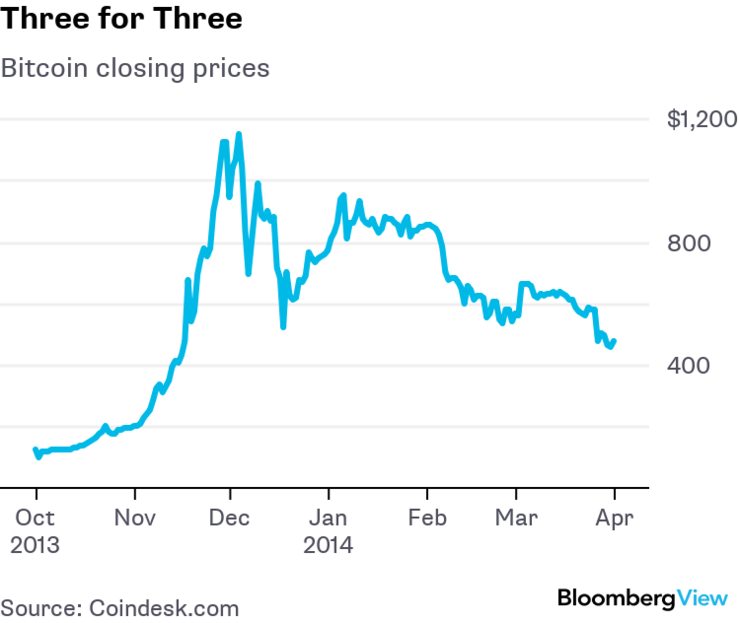

The recent Bitcoin bubble wasn’t the first, and it might not be the last. Once in 2011 and twice in 2013, the price soared and then crashed:

.png)

Each peak was bigger than the last. If you think there will be another, even bigger bubble somewhere down the line, then maybe any losses you took in the recent bubble may be made whole in time.

Why has Bitcoin been subject to repeated bubbles? One reason is lack of liquidity -- since relatively few people owned and traded the cryptocurrency in years past, even a small surge of buying could push the price up dramatically, and even a modest pullback could send it crashing.

A second reason is that Bitcoin was, at least until recently, a new asset. Speculators had no real idea how many potential cryptocurrency investors were out there. Economic theory shows that this can easily lead to an overshoot, where even rational investors temporarily push an asset’s price beyond its long-term sustainable value.

But there’s a third reason for Bitcoin’s bubbliness -- it was hard to bet against it.

Basic finance theory says that if there’s no way to invest and profit from an asset's decline, the price is determined by the most optimistic buyer. If some traders think Bitcoin is overpriced, but have no way to bet on their belief, they will just sell their stake and sit out of the market. Everyone who remains will be an optimist, and they will buy Bitcoin for the high price they believe it’s worth.

This mechanism is a key part of almost every theory of financial bubbles. A famous 1978 paper by J. Michael Harrison and David Kreps showed how without short-selling, differing levels of optimism and pessimism would cause even rational agents to push asset prices above fundamental values. A later model of bubbles and crashes by Dilip Abreu and Markus Brunnermeier also featured a limit on short-selling, as did another by Jose Scheinkman and Wei Xiong. In a short sale, an investor borrows an asset such as a stock or bond and sells it, hoping to buy it back for less to return to the lender and pocket the difference as a gain.

In 1997, Andrei Shleifer and Robert Vishny proposed to make this sort of constraint, which they grouped under the general heading of “limits to arbitrage,” a unifying theory of financial market failures. Research on just why and how smart, well-informed traders are unable to cancel out bubbles continues to this day.

Limits to arbitrage can help explain why Bitcoin has been so bubble-prone. Until recently, it was easy enough to take a long position, but expensive and risky to bet against the cryptocurrency. Things really changed in December, when U.S. regulators allowed the trading of Bitcoin futures. That move came in the middle of a historic runup in the price of Bitcoin and other cryptocurrencies. But as soon as futures contracts began to trade, an interesting thing happened -- futures prices suggested that Bitcoin’s growth would slow.

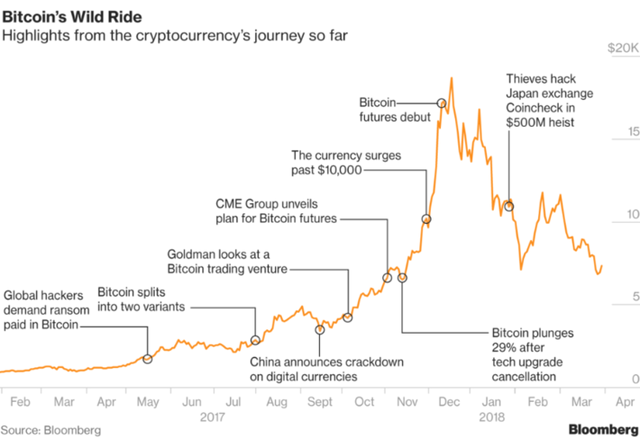

What happened next is historic. Bitcoin’s price crashed from a high of about $19,000 to less than $7,000 as of the writing of this article:

.png)

Was this a coincidence? Maybe. The huge surge in demand for Bitcoin both inflated the bubble and caused a demand for a futures market. But the timing of the crash, right after the introduction of futures markets, is eerie. It mirrors the result of a 2006 paper by economists Charles Noussair and Steven Tucker, who introduced a futures market into a trading experiment:

We find that when futures markets are present, bubbles do not occur in [our experimental asset] markets. The futures markets seem to reduce the speculation and the decision errors that appear to give rise to price bubbles in experimental asset markets.

A few students trading an imaginary stock in a laboratory isn’t the same as millions of real people trading tens of billions of dollars worth of Bitcoin. But this is a case when theory, lab experiments and practical experience align to a spooky degree. The housing bubble is another example where betting against the asset in question was extremely difficult.

This suggests that there’s a good and easy way for regulators to reduce the incidence of bubbles. Whenever a new asset is created or a bunch of new investors enters the market, allow more futures trading and other exchanges that let pessimists publicly register their pessimistic beliefs. That won’t totally prevent all bubbles -- the late 1990s technology stock bubble, for instance, happened in spite of the existence of stock futures markets.

But it would certainly help. Keeping pessimists out of the market is a recipe for repeated bubbles and crashes, as overoptimistic speculators rampage unchecked. Given a level playing field, the bears can restrain the bulls

Hi @ranawali

Excellent article. I subscribed to your blog.

I will be grateful if you subscribe to my blog @dreladred

Good luck to you!