China put a Ban on Bitcoin

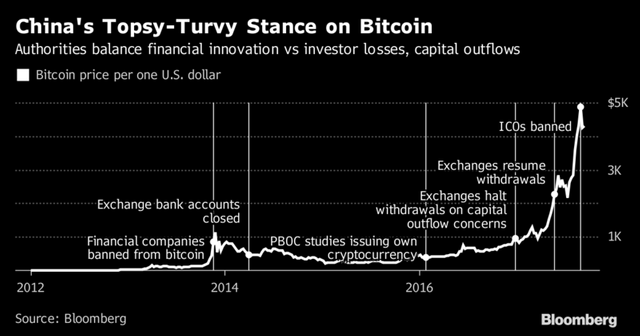

China plans to ban trading of bitcoin and other virtual currencies on domestic exchanges, dealing another blow to the $150 billion cryptocurrency market after the country outlawed initial coin offerings last week.

The ban will only apply to trading of cryptocurrencies on exchanges, according to people familiar with the matter, who asked not to be named because the information is private. Authorities don’t have plans to stop over-the-counter transactions, the people said. China’s central bank said it couldn’t immediately comment.

Bitcoin slumped on Friday after Caixin magazine reported China’s plans, capping the virtual currency’s biggest weekly retreat in nearly two months. The country accounts for about 23 percent of bitcoin trades and is also home to many of the world’s biggest bitcoin miners, who use vast amounts of computing power to confirm transactions in the digital currency.

“Trading volume would definitely shrink,” said Zhou Shuoji, Beijing-based founding partner at FBG Capital, which invests in cryptocurrencies. “Old users will definitely still trade, but the entry threshold for new users is now very high. This will definitely slow the development of cryptocurrencies in China.”

While Beijing’s motivation for the exchange ban is unclear, it comes amid a broad clampdown on financial risk in the run-up to a key Communist Party leadership reshuffle next month. Bitcoin has jumped about 600 percent in dollar terms over the past year, fueling concerns of a bubble. The People’s Bank of China has done trial runs of its own prototype cryptocurrency, taking it a step closer to being the first major central bank to issue digital money.

“There has been a general tightening of the screw on regulating financial and monetary conditions,” said Mark McFarland, chief economist at Union Bancaire Privee SA HK in Hong Kong. “All of these things suggest a longer term process of tightening scrutiny of activities that aren’t in the normal sort of monetary realm.”

OKCoin, BTC China and Huobi, the country’s three biggest bitcoin exchanges, said on Monday that they hadn’t received any regulatory notices concerning bans on cryptocurrency trading. All three venues reported transactions on Monday, with bitcoin rising 7.6 percent on OKCoin as of 5:09 p.m. local time.

Read more about last week’s ban on initial coin offerings here.

While bitcoin users will still be able to trade cryptocurrencies in China without exchanges, the process is likely to be slower and come with increased credit risk, analysts said.

The exchange ban is unlikely to have a major impact on the prices of cryptocurrencies globally because venues outside China will continue trading, according to FBG Capital’s Zhou. The country’s role in the bitcoin market had already started shrinking in recent months as authorities tightened regulation. At one point, exchanges in China accounted for more than 90 percent of the world’s bitcoin transactions.

The bigger risk for global traders may be the massive rally in bitcoin prices, according to McFarland.

“Whenever you start to hear about Hong Kong taxi drivers becoming millionaires from buying bitcoin, you start to think this is not necessarily driven by fundamentals,” he said. “So you will get quite substantial pullbacks at some point.”

credit: www.bloomberg.com