Ten things for blockchain startups to remember

Blockchain is by far the most revolutionary model to emerge in the last decade. It has the potential to disrupt entrenched players in industry and governments. It also threatens to force us to relearn and reinvent ourselves in adapting to a brave new world. The very concept of decentralized control and autonomous organizations are indigestible to a populace that has been fed a steady diet of centralized control since childhood.

I personally want blockchains to succeed because they provide a refreshing look at a landscape dominated by the fortunate few. But we have to face the fact that blockchain companies need to traverse a tricky and torturous path to get there.

There appears to be almost 3000 blockchain companies across the world. All of them may not be developing blockchain directly or may be side loading blockchain into their applications. But it is still a huge number. Shades of the dotcom bubble waiting to happen?

I am leapfrogging on this techcrunch article.

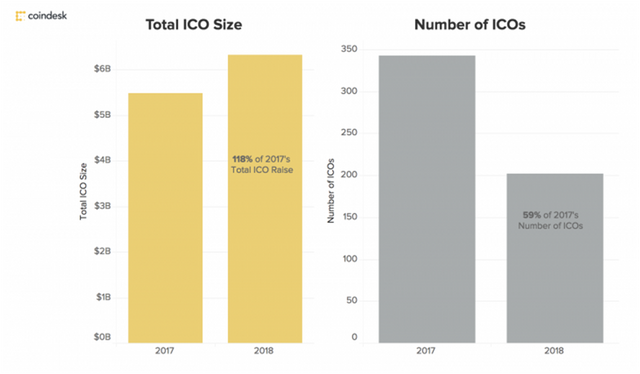

The number of ICOs on the other hand shows virtually no signs of abating:

source: https://www.coindesk.com/6-3-billion-2018-ico-funding-already-outpaced-2017/

In yet another disquieting fact, it is found that 70% of all startups fail and almost 98% of all hardware startups crash and burn! It appears that there are some extraordinary precedents.

Startup challenges are generally well known

We have all been in startups at some time or the other. Some have risen above mediocrity and others have failed. But the challenges for any startup are fairly obvious:

- Business models that we chase got disrupted by another entrant or a well established player

- Cash runs out

- Teams split apart or don’t work well together

- Product or service does not ring a bell with its potential customers

- Companies are poorly managed

- Core problem being solved had no financial takers

I personally think that public blockchains have learnings that are completely different from other startups. In order for them to break through, they must realize rapidly that their core challenges are inordinately more taxing.

The word blockchain in this context specifically refers to public blockchain startups similar to Ethereum, BitFinex, Kik, Poloniex, Gemini, Monero, etc. Since crypto currencies are well understood, let us omit blockchains which are pure play currency providers like Bitcoin, Litecoin and their ilk.

The challenge of being a public blockchain company

Henrik Ibsen once said:

A community is like a ship; everyone ought to be prepared to take the helm

Blockchain companies have to understand that leadership is not by committee but by rotating the responsibility. However that is still the easiest challenge they will face.

Aligning the community is critical

source: cryptocoinmastery

Most blockchain companies evolve as communities. These communities sustain the company by offering a valued service to one another. If the business model of the company is centered around such communities then it becomes imperative to find out whether it is sustainable in the long term.

The biggest risk to blockchain success is a major disagreement in the community followed by chain splitting hardforks.

Remember that most people try different things at different times. E.g. Open Bazaar is a P2P buying/selling network. There is an assumption made that people would like to buy from each other in the long term. This has to be validated in the years ahead but the problem is evident. There has to be a very strong compulsion for people to keep on trading with each other. This will limit the number of products and peer types that will interact with each other.

There is also a pervasive danger in closed communities and it is that familiarity breeds contempt. As people get closer to each other, they will find out reasons to hate or distrust each other. Blockchain companies are more permeable to behavioral anomalies.

It works if the focus is on creating niche trading communities that see tremendous value in each other. E.g. the entire Nuclear Suppliers Group (NSG) can be a very effective blockchain based P2P community! Currency exchanges are also a natural fit. Decentralized gaming is perfect for a public blockchain.

How decentralized is your blockchain?

source: cartoons by Miles

Almost all blockchain companies attract an initial set of members based on the premise of decentralized ownership. But in reality less than one percent ends up owning 60% of the hashrate thus controlling the blockchain.This is even more predictable in Proof Of Stake (POS) models where 1% have almost 90% stake in the company. When this happens the bigger stakeholders get all the rewards.

Bitmain is nearing 51% hashrate . 3 miners account for 61% hashrate in Ethereum

People are realizing that such a situation is an exact replica of monolithic companies that already exist. Blockchain companies need passion and conviction to pull off the impossible. They are built on the hope of causing massive disruptions to existing processes. But the lopsided ownership results in a negative impact across the board.

Each of these companies will mine a set of tokens and divide it amongst the initial founding team. The next set of mined tokens is allocated to the general public. Who might the general public be? They are composed of initial investors who buy tokens or early stage recruits who are awarded them.

In other words the company will reward early believers and it is no different from any other company out there. This results in disproportionate holdings which can never be rolled back. Given that blockchain communities have fierce socialistic ambitions, it is particularly galling to note these trends.

Blockchains are making people very rich too:

Inflation is one of the solutions that could work in the long term even though it is frowned upon by most blockchain gurus. The other way is to have a mechanism wherein a percentage of stake is constantly diluted based on sustained contribution. This mechanism will work on well ordered communities.

Developers have an inordinate influence on the blockchain

This is a byproduct of developing bleeding edge technologies made worse by aggressive self promotions. The shortage of blockchain technology experts coupled with yet to be discovered business models meant that developers rule the roost in all decision making.

In traditional companies, one always felt that developers would create a sense of balance missing in rampant sales/marketing driven decision making. In blockchains, the lack of business nous makes it a very difficult journey.

Since most blockchains are governed by larger stakeholders, the remaining members have very little say in business direction and execution. A core group of stakeholders filled with developers and architects make most of the decisions.

There are many blockchains having infantile business plans and like Icarus are winging themselves closer to self immolation.

It is not a bad idea to cull a few successful mid level executives from larger companies. They are malleable and will transfer their learning rapidly. It also helps that they will be on the growth curve looking for better opportunities. The right industries to target are manufacturing and architecture because they have a firm grasp of the blue collar ethic that is required to run a blockchain.

Quality of service is harder to provide

source: data virtualization blog

People do not realize how difficult it is to provide quality services in a decentralized model. Let us consider the case of Golem which is offering compute farms using public infrastructure. Golem promises world class rendering by spreading jobs across thousands of cores owned by individuals or datacenters across the world.

Even though Golem has software that will scan the machines and validate them before forking out rendering tasks, imagine the sheer diversity in play. There is no guarantee of finding machines with required configuration at all times. Software changes or upgrades could cause incompatibilities.

The point to be made is that even though software will try and sanctify environments, the reality is that nodes themselves are not under singular control. Accountability will suffer because taking responsibility is a rare characteristic.

If you add wanton acts of destruction from disgruntled members then the task of sustaining quality of service becomes all the more difficult. Network and power infrastructure are not identical in different parts of the world and this will add new wrinkles into the game plan.

Blockchain companies have to invest in processes for ensuring quality just like any other manufacturing or service organization. Vigilance must become a fundamental principle behind the offering. Human and technological oversight will need to emerge as a triaging mechanism to ensure conformance.

Decentralized clouds are more prone to security issues

We are all aware that centralized data repositories are prone to data breaches because the profit in such an initiative is very high. You have companies that are making money out of data and hence ransomware proliferates.

But that does not mean that decentralized blockchain nodes are without their own security problems. In decentralized clouds (like Dfinity, Aelf, Storj…) jobs are generally split to attain anonymity and then distributed across nodes.

As of today we have mining nodes, consensus nodes and bookkeeping nodes in a 3-tier architecture. This puts an enormous amount of stress on developers to ensure that jobs that run on decentralized clouds are secure and safe from snooping.

If you encrypt data then key management across 1000s of nodes becomes difficult. If you just slice data up and distribute it then a particularly smart malware can snoop and create an identifiable pattern over time. After all, centralized intrusion detection does have its benefits.

Even though the ledger protocol assures sanctity, the Dapp that is built on top is far more vulnerable.

It is critical to build host based intrusion detection systems right from the start. A high grade audit framework is an absolute necessity. Equally critical would be to build application level end point compliance support.

Dapps can be gamed too

The community power of blockchain also works against it. Human beings have an innate sense of how to circumvent a rule that was supposedly inviolable. We have been doing it for centuries and we will never stop as long as there is something to gain.

Voting which is a pillar of all blockchain communities can be gamed. Members can enact quid pro quos to reward each other. The infamous circle jerking voting paradigm is very hard to stop because it is unclear where it begins and ends. Voting bots will ensure massive rigging of financial reward strategies. In proof of stake models, delegation is a curse for it melts down into abdication of responsibility.

A painful realization that all members arrive at eventually is when they realize that large stakeholders will manipulate rules to favor their returns. It should not be surprising but it usually comes as a shock to most newbies.

Even one token one vote systems can enable colluding groups to take control of a blockchain. Mining pools absolutely do not help!

In other words, real world meets blockchain!

Stake based voting should definitely be discarded because they make the blockchain undemocratic. All voting will then evolve to simple majority with weights to compensate for shortfall of votes. It is highly appropriate to enforce voting quotas for different kinds of decisions.

Trust is not a given in every situation

Blockchains are built on the premise of a transparent ledger but that does not guarantee building of trust. It just makes the reasons to mistrust highly visible. Conceptually we assume that since everyone has something to lose, they will not enter bad data or try to fool the system. In some cases, transparency itself may not be needed. Let us consider a few examples:

- Would you like to know that a doctor prescribed for a patient? It does not matter whether the prescription itself is invisible, the knowledge of that exchange is itself enough to set alarm bells ringing

- A smart contract allows an architect to be paid when his work is done. But to build automated verification of work is not in the scope of the blockchain. It can only deal with the data that is input and it is entirely possible that the architect has lied. In order to catch his lie, we would have to implement a system that collects data from the materials supply chain, visual inspection data, material quality test and so on

- You sold your real estate property on a blockchain. It was a distress sale and hence you sold it at a very low price. Would you really want this known? People do not realize that as long as some aspect of the transaction is known (say price), then a snoop can always correlate this with civic records

When you choose your use cases, it is wise to think of the system that already exists outside of the blockchain. For blockchains to work, they must own the entire functionality and not merely be enablers. E.g. Going back to the real estate example, if the blockchain manages all broker commissions for a particular county, then it is a fully contained problem and has a high chance of being successful.

Creating the framework to handle legal problems in the future

source: Dilbert cartoons

Blockchain is a vast decentralized community. When things go wrong, who will we hold responsible? Blockchain companies are registered and have a set of legal functionaries but who does the public hold responsible? Unlike a regular company, there is no hierarchical decision making. The community votes for policy changes and because of that the consumer of a service might be affected.

Let us assume that a service has failed because of an errant member or bad hardware provided by a decentralized node. E.g. your interplanetary file provider is not able to bring your income tax return back and the consumer is suing! Can we transfer accountability to an individual? Will a blockchain represent itself as a set of peers or as a real company and front all failures?

At some point, external legal recourse will be sought and blockchains cannot deal with problems internally. Since decentralized communities cannot pass accountability around like they do in centralized organizations, it becomes imperative to be prepared to deal with governments/courts even to solve internal problems.

Arbitrations inside the company may turn to legal recourse and for any community that is not great news! Imagine if the company is spread across a 100 countries, the problem multiplies exponentially.

A process and a framework to redress internal grievances is absolutely required. If that does not exist, external legal intervention becomes a painful reality. There must be protocols to elect witnesses in a round robin manner who can testify to court. Jurisdictional compliance must be followed. Legal fees need to be part of all transactions so that a legal fund can be setup to handle future problems.

Business models must be sound and rely on collective value

Many companies tout the presence of blockchain itself as a revolutionary business model.

I have seen many blockchain companies that forget that they are a community which opted to work together. Any value that they bring to their customers must arise from this collective wellspring of initiative and efforts.

The business model problem is not new. I see blockchain startups that want to develop blockchain frameworks to enable other non-blockchain based companies to thrive.

Why is this bad?

Each blockchain company has to discover a business model that is weaving its members and customers together. If you get cut off from the end customer experience, then the odds mount against you. Such an offering is for a more mature market where blockchain experience has been absorbed and now there is a need to replicate that specific experience without additional effort.

This is not to say that Ethereum will not become a big success but the days of Ethereum being a startup is long gone.

If Uber were built on a blockchain, would things be different? Would you suddenly feel that there is this vast community of drivers wanting to offer the best service possible? If profits were distributed amongst Uber drivers, would you find friendly drivers who are safe, secure and always willing to go the extra mile because it is their own company? If you had a problem with a driver, would another driver drop by and try to resolve the matter? If this is not true, then there is very little point in building a blockchain taxi cab service!

The mission of a blockchain company must be offer premium service by using the collective abilities of its members. The vision must be to offer democratically enabled services that cannot be offered by monolithic organizations.

Just doing a blockchain is not disruptive enough

Blockchains need to disrupt status quo in order to survive. They cannot be just another database or ledger that is open to the public. There needs to be a strong value proposition beyond buzz words like transparency, distributed ledger, decentralized trust, etc. At a minimum, the disruption must rearrange traditional relationships, create brand new revenue opportunities or make an existing business model redundant.

There are many blockchain companies that are born with the belief that replicating the world view within a blockchain will make it the magic elixir. *But we all know that is just the sound of old wine being poured into a swanky new bottle.

Perhaps it is trendier to say old coke in a new can?

How would it be if we had blockchain versions of Disqus, Taboola, Amway, FaceBook or Google? We know the functionality is not new. We are equally aware that the user experience is similar. The only difference would be the way blockchain would work under the covers, isn’t it?

As I write, there is a Ticketmaster on blockchain and I cannot understand why.

It is imperative that blockchains focus on quantifiable disruption. It definitely seems sanctimonious to criticize a business model until proven otherwise but the reality of an omelet made without breaking eggs stares at us dead in the face.

If you can safely eliminate middle men then it is an obvious disruptor. If you can create a whole new class of middle men, that is disruption too. If you keep the focus on enabling relationships between people who had never met before but are now willing to work together to create a brave new world, then you will have arrived.

Conclusion

Blockchain companies should focus on core values of peer to peer relationships and evolutionary business models. There are many challenges that they face which are quite different from traditional companies.

Blockchain’s real value is in disrupting B2B relationships. It allows smaller companies to leverage cryptocurrency and create a scaleout backend that can rival larger companies at very little cost. If we see enough companies focusing on this value, then we will see a gradual disintegration of larger enterprise companies bringing parity to the world. But if blockchain startups focus too much on the consumer then they will fight existing consumer giants and burn up on reentry.

please share your comments for i would love to read them

A scholarly work, @adarshh! I have been focusing on the "how" of a blockchain and this helps me understand the "why" of using one. Now, it's obvious to me that it is not a universal solution.

You get extra points for including Dilbert!

thank you @willymac for those gracious words. you are right, that blockchain is not a solution for everything. however if applied wisely, it can really make a difference. I guess that is how it is for all technologies.

@adarshh Thank you for not using bidbots on this post and also using the #nobidbot tag!